Anything that gets journaled is essentially keeping a record of something in an organized manner. For easy payroll management, it’s often necessary to maintain journal entries.

But has finance management ever seemed easy to anyone?

Well, we’re making it easy for you now!

Go through the guide below to learn about accounting example journal entries and the process of transactions in accounting journals.

Table of Contents

What Are Journal Entries In Accounting?

The record of a business transaction in the general ledger is considered as the answer to what is a journal entry. For every financial exchange moment made by your business, there has to be a journal entry to track transaction details. These entries are vital for ensuring that the balance sheet is accurate, the income statement is properly updated, and overall financial reporting is correct.

A journal entry typically consists of the following components:

- Date of the transaction in the accounting journal

- Accounts affected

- Debit and credit amounts

- A brief description or memo explaining the transaction

The ultimate goal of journal entries accounting is to keep the accounting books balanced. The accounting equation, Assets = Liabilities + Equity, should hold after every entry is made.

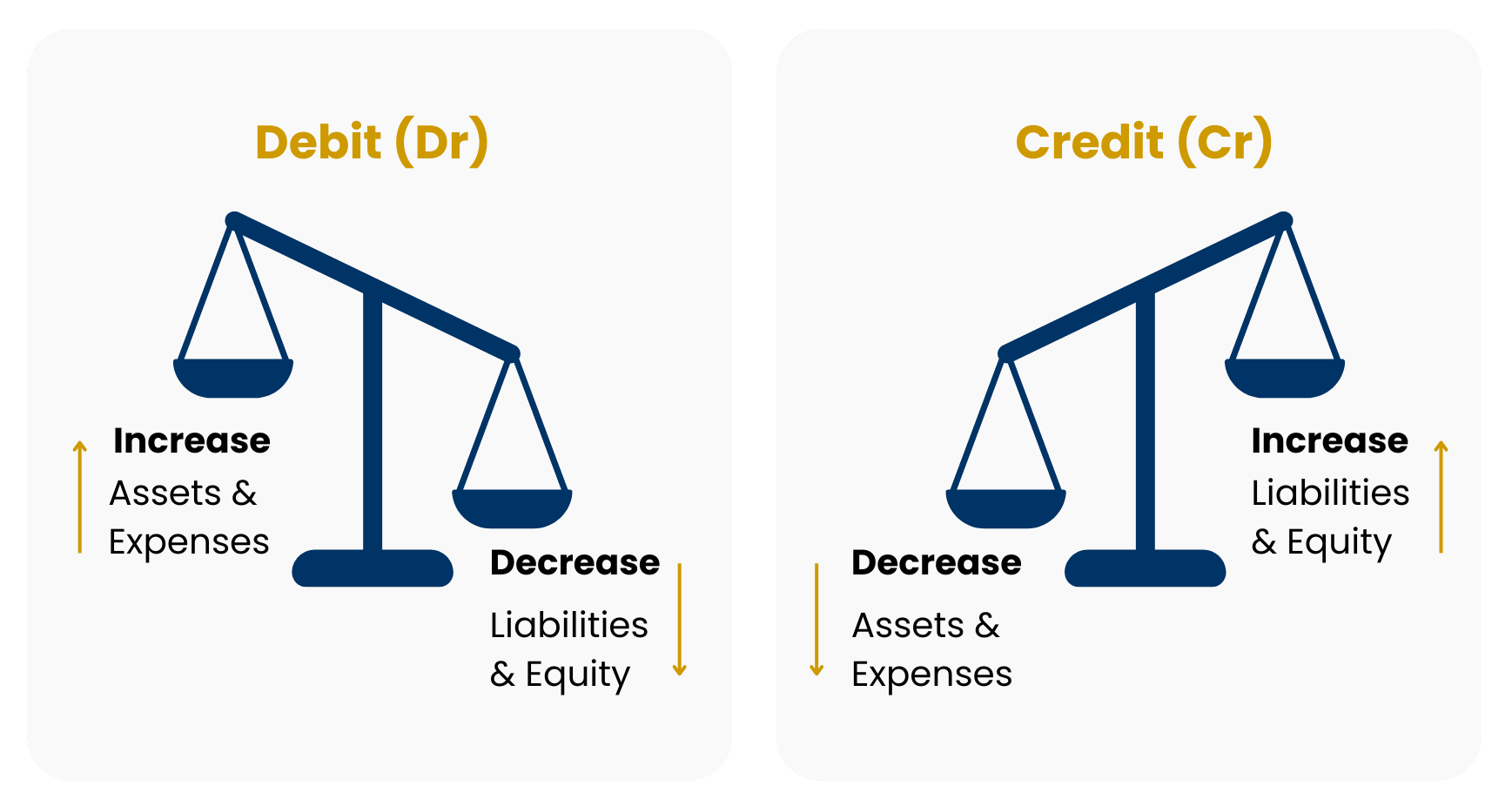

Double-Entry Bookkeeping: The Foundation of Journal Entries

Double-entry bookkeeping is the backbone of journal entries. Every financial transaction impacts at least two accounts—one is debited, and the other is credited.

This system ensures that the accounting equation stays in balance:

Assets = Liabilities + Equity.

At the peak of this system along with bookkeeping journal entries examples are debits and credits:

- Debits (DR): Increase asset accounts and decrease liability and equity accounts.

- Credits (CR): Decrease asset accounts and increase liability and equity accounts.

Bookkeeping journal entries examples:

If you buy a $500 piece of equipment with cash, you’re adding to your assets (equipment), but reducing another asset (cash). Both accounts must be adjusted:

- Debit: Equipment $500 (increase in asset)

- Credit: Cash $500 (decrease in asset)

This method provides a complete, error-resistant way to track financial transactions. Using double-entry bookkeeping, you can easily spot discrepancies, as every debit must have a corresponding credit.

Need external help with journal entries?

Whether you’re a small business owner or an aspiring accountant, maintaining journal entries is a need. If you’re looking for professional accounting support, get in touch with us today!

Also Read: Understanding Debits And Credits: A Visual Guide For Beginners

Most Common Types of Journal Entries

Journal entries are not all the same, and different types of transactions require different types of journal entries accounting.

Here are the main types with accounting example journal entries:

1. Simple Journal Entry

A simple journal entry is the most straightforward type of journal entry. It involves only two accounts i.e., one account is debited, and another is credited.

Example:

If you pay rent for $500, the simple entry would be:

- Debit: Rent Expense $500

- Credit: Cash $500

2. Compound Journal Entry

A compound journal entry involves more than two accounts. It’s used when a transaction affects multiple accounting example journal entries, making it a bit more complex than a simple entry.

Example:

Let’s say you purchased supplies for $1,000, part of which was paid with cash and the rest on credit. The compound entry would look like this:

- Debit: Supplies $1,000

- Credit: Cash $600

- Credit: Accounts Payable $400

3. Adjusting Journal Entry

An adjusting journal entry is made at the end of an accounting period to update accounts. These adjustments may be necessary for items like accrued expenses, earned revenue, or depreciation, ensuring the books reflect the correct balances.

Example:

At the end of the month, if your business owes $100 in utility expenses but hasn’t paid yet, the adjusting entry would be:

- Debit: Utility Expense $100

- Credit: Accounts Payable $100

Adjusting entries is critical for matching revenues and expenses to the correct accounting period.

4. Reversing Journal Entry

A reversing journal entry is made at the start of a new period to reverse an adjusting entry made in the previous period. This type of accounting example journal entries is used to correct temporary changes or clear out certain accrued balances.

Example:

If an adjusting entry was made for accrued salary expenses in the previous period and it was paid in the new period, you would reverse the initial adjusting entry:

- Debit: Accounts Payable $100

- Credit: Salary Expense $100

Reversing entries helps ensure that financial records remain accurate and reflect actual cash flows.

5. Closing Journal Entry

A closing journal entry is made at the end of an accounting period to transfer temporary account balances (like revenues and expenses) to permanent accounts, such as the retained earnings account. This prepares the books for the next accounting period.

Example:

At the end of the year, if your business had revenue of $50,000 and expenses of $30,000, you would close those accounts into retained earnings:

- Debit: Revenue $50,000

- Credit: Retained Earnings $50,000

And to close the expense accounts:

- Debit: Retained Earnings $30,000

- Credit: Expense Accounts $30,000

Closing entries reset temporary account balances to zero in preparation for the new period.

Also Read: A Complete Guide to Goodwill in Accounting for Business Owners

Steps to Record a Journal Entry

Making bookkeeping journal entries examples doesn’t have to be overwhelming. Here’s a simple breakdown of the process:

1. Identify the Transaction: This step involves understanding the financial event that took place. Was money spent? Was a service provided? Identify which accounts are impacted.

2. Determine the Accounts: Next, determine which accounts need to be debited and credited. A good rule of thumb is:

-

-

- If the transaction in an accounting journal involves a cash outflow (like buying something), it will likely involve a debit to an expense account and a cash credit.

- If the transaction in an accounting journal involves revenue (like sales), you’ll debit accounts receivable and credit sales revenue.

-

3. Complete the Journal Entry: Write the journal entry, including the date, accounts, amounts, and a brief description. Make sure your debits and credits are balanced.

4. Post to the General Ledger: After the journal entry is made, it is posted to the general ledger, where it will eventually appear in the financial statements.

Tips for You: Double-check your entries! Mistakes can lead to discrepancies in your financial reports, which can affect decision-making and business strategies.

Let’s Wrap!

Specializing in journal entries accounting is an important skill in the field. By understanding the basics like debits and credits, you can ensure your financial transactions in accounting journals are always accurate. Whether you’re handling personal finances or running a business, getting an answer to “What is a journal entry?” can be your key to success.

If you need to improve your accounting practices, connect with a professional accountant from Orbit Accountants. Reach out now and see for yourself!

Frequently Asked Questions

1. What is the purpose of a journal entry in accounting?

A journal entry records every financial transaction, ensuring that all business activities are properly documented and categorized. It’s the backbone of accurate accounting, keeping your books balanced and your financial statements in check.

2. What are the basic components of a journal entry in accounting?

A journal entry includes the date, accounts involved, debit/credit amounts, and a brief description of the transaction in an accounting journal.

3. How do journal entries affect financial statements?

Journal entries accounting update your balance sheet, income statement, and cash flow statement. By tracking every transaction, they ensure that your financial statements reflect the true state of your business—accurate and up-to-date.

4. How do accounting journal entries work?

Journal entries accounting work by following the rule of double-entry bookkeeping: for every debit, there’s a corresponding credit. This system keeps the accounting equation balanced (Assets = Liabilities + Equity).