It’s this term- “goodwill” that gets most business owners talking about themselves during critical events like buying or selling a firm. Beyond the business transfer, however, understanding what is goodwill in accounting offers valuable insights into the elements that truly make a business worth more than just what’s shown on the balance sheet.

If you’re a business owner preparing for a merger or acquisition—or simply curious about how goodwill fits into your company’s financial story—this guide is for you. We’ll break it down, professionally, and with just enough punch to keep things engaging.

Here’s your revised Table of Contents for the goodwill blog, without the FAQ questions and the section “Why Goodwill Matters to Business Owners”:

Table of Contents

What is Goodwill in Accounting?

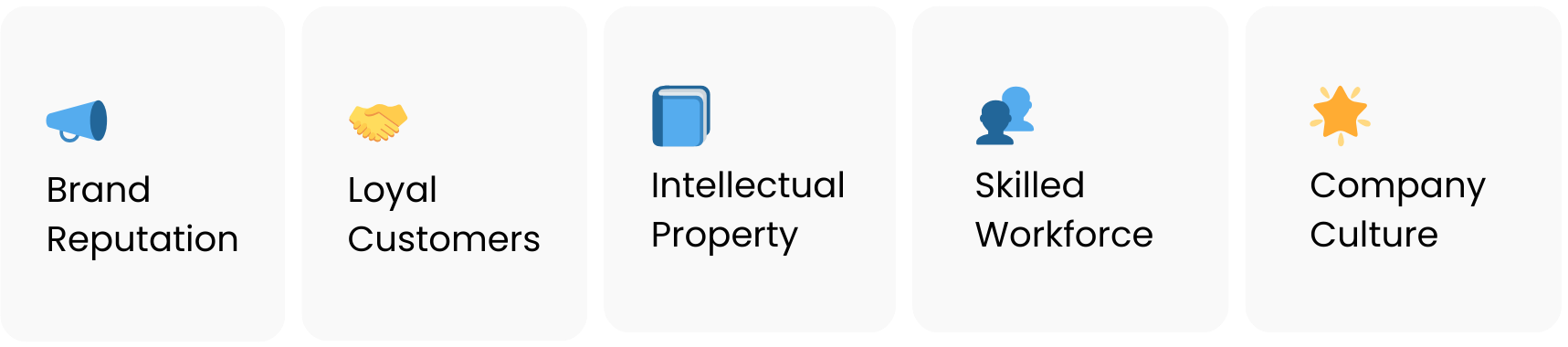

Goodwill, in accounting terms, is what you record when one business acquires another for more than the fair market value of its tangible assets and liabilities. This “extra” amount isn’t random—it’s the price you pay for things that aren’t listed on a spreadsheet: brand reputation, loyal customers, intellectual property, and even the vibe of a well-oiled team.

You can think of goodwill as the silent superstar of your business—it doesn’t show up directly in revenue or inventory, but it plays a major role in long-term success.

And here’s the catch: goodwill only appears on a balance sheet when there’s been a business acquisition. If you’ve built your company from scratch and know that your brand alone is worth six figures, that value doesn’t get recorded as goodwill until someone buys your business for more than its net asset value. That’s what is goodwill in accounting—an acquired, not self-generated, intangible asset.

Are you currently managing your bookkeeping in-house?

Examples of Goodwill in Accounting

Let’s say Company A acquires Company B for $1 million. Company B’s assets, after accounting for liabilities, are worth $750,000. That extra $250,000 paid? That’s goodwill.

Goodwill = Purchase Price – (Fair Market Value of Assets – Liabilities)

Using the numbers above:

$1,000,000 – $750,000 = $250,000 recorded as goodwill.

This isn’t just accounting fluff—it’s a recognized component of valuation. Investors and stakeholders often consider these examples of goodwill accounting when evaluating acquisition decisions.

Here are more examples of goodwill accounting in action:

- Tech acquisitions: Big tech firms buying start-ups for user base and brand reputation.

- Retail/franchises: Paying more for a local outlet due to loyal customers and brand equity.

- Hospitality: A hotel bought for its great reviews and location, not just its building value.

What is Goodwill on a Balance Sheet?

Now that we’ve understood how goodwill comes into play, let’s talk about what is goodwill on a balance sheet.

Goodwill appears as a non-current intangible asset. It’s recorded only after an acquisition and reflects the intangible worth paid over the company’s net assets.

What’s unique about what is goodwill on a balance sheet is that it doesn’t get amortized like some intangibles. Instead, it’s tested annually for impairment. If goodwill is found to have lost value—maybe due to a reputational hit—it must be written down, and that write-down becomes an expense on the income statement.

So, when you ask what is goodwill on a balance sheet, remember:

- It’s an asset, not a cost.

- It reflects acquired intangible value.

- It doesn’t vanish with time but can be impaired when its value drops.

Also Read: What is Retained Earnings? Formula, Calculation, and Examples

Why Goodwill Matters to Business Owners?

For entrepreneurs and business owners, goodwill can be a game changer in more ways than one. Here’s why:

- It Reflects Brand Equity: A good name takes years to build. That trust, recognition, and reputation are often why buyers pay more than the bookkeeping.

- It Adds to Negotiation Power: Knowing your goodwill value gives you leverage during sales or acquisition talks.

- It Affects Future Financials: Impairments can lead to sudden dips in reported income, impacting loan terms, investor interest, and company valuation.

- It Signals Value Beyond Assets: Not everything that counts can be counted. Goodwill captures what the spreadsheets can’t.

How to Calculate Goodwill in Accounting?

Let’s now break down how to calculate goodwill in accounting, step-by-step.

The basic formula is:

Goodwill = Purchase Price – (Fair Value of Assets – Liabilities)

But while this sounds easy, it’s rarely that simple. You’ll need to accurately assess asset values, account for any hidden liabilities, and perform thorough due diligence. Misjudgements can lead to inflated goodwill and future financial headaches.

Whether you’re buying a small business or overseeing a larger M&A deal, always consult a professional accountant or valuation expert when figuring out how to calculate goodwill in accounting.

Also, how to calculate goodwill in accounting comes into action for reporting and taxation purposes—it’s not just about balancing your books but also presenting a trustworthy image to investors and regulators.

Examples of Goodwill in Practice

- Tech Startup Acquisitions: When a major software company buys a niche startup, it’s rarely just for code. It might be for the talent, user base, or industry position—the kind of value that gets recorded as goodwill.

- Franchises and Retail: Purchasing a franchise with a loyal customer base and local popularity often includes paying more than the cost of inventory and fixtures. That additional value? Goodwill.

- Hospitality Industry: A well-reviewed hotel in a prime location, even if not luxurious, may command a premium due to positive public perception, repeat guests, and strong management.

What Goodwill is Not

It’s important to clarify what goodwill isn’t:

- It’s not a physical asset you can sell.

- It’s not amortized (unless under certain private entity frameworks).

- It’s not internally generated.

That means you can’t just assign goodwill to your own business because you believe it’s worth more—it must come from a purchase.

Journal Entry for Goodwill

At the time of acquisition, the journal entry might look like this:

Dr. Assets (at Fair Market Value)

Dr. Goodwill (for the excess amount)

Cr. Liabilities (assumed from seller)

Cr. Cash or Payables (purchase price)

This ensures that the purchase is accurately reflected, balancing both tangible and intangible contributions to the company’s value.

Also Read: Everything You Need To Know About Journal Entry In Accounting

Frequently Asked Questions:

What does goodwill mean in accounting?

Goodwill refers to the intangible value a company gains when acquiring another business for more than the fair market value of its net assets. It includes brand reputation, customer relationships, and other non-physical assets.

Is goodwill an expense or income?

Neither. It is an intangible asset. However, if it becomes impaired, the loss is treated as an expense.

What is the journal entry for goodwill?

The journal entry involves debiting assets and goodwill while crediting liabilities and the purchase amount.

What is an example of goodwill?

Paying more for a business due to its reputation, loyal customer base, or strong employee culture.

Why is goodwill considered an asset?

Because it represents a quantifiable benefit expected to bring future economic value, despite lacking physical form.

Disclaimer: This blog is intended for informational purposes only and does not constitute financial, legal, or accounting advice. For guidance tailored to your specific situation, please consult a qualified professional.