Starting a business comes with a million to-dos. But one of the most important decisions—one that impacts your taxes, legal protection, and even how people perceive your brand—is choosing your business entity type.

If you’re not sure what that even means, you’re not alone. Let’s walk through it together.

Table of Contents

What Does “Entity Type” Mean?

In simple terms, your entity type is the legal structure of your business. It’s how the IRS, your state, and pretty much every government body sees your company.

This entity type meaning affects things like:

- How do you pay taxes?

- Whether your assets are protected?

- How are you allowed to raise money?

- What paperwork you’ll need to file every year?

In short, the type of entity you choose isn’t just about compliance—it’s about protecting your business and setting yourself up for growth.

Are you currently managing your bookkeeping in-house?

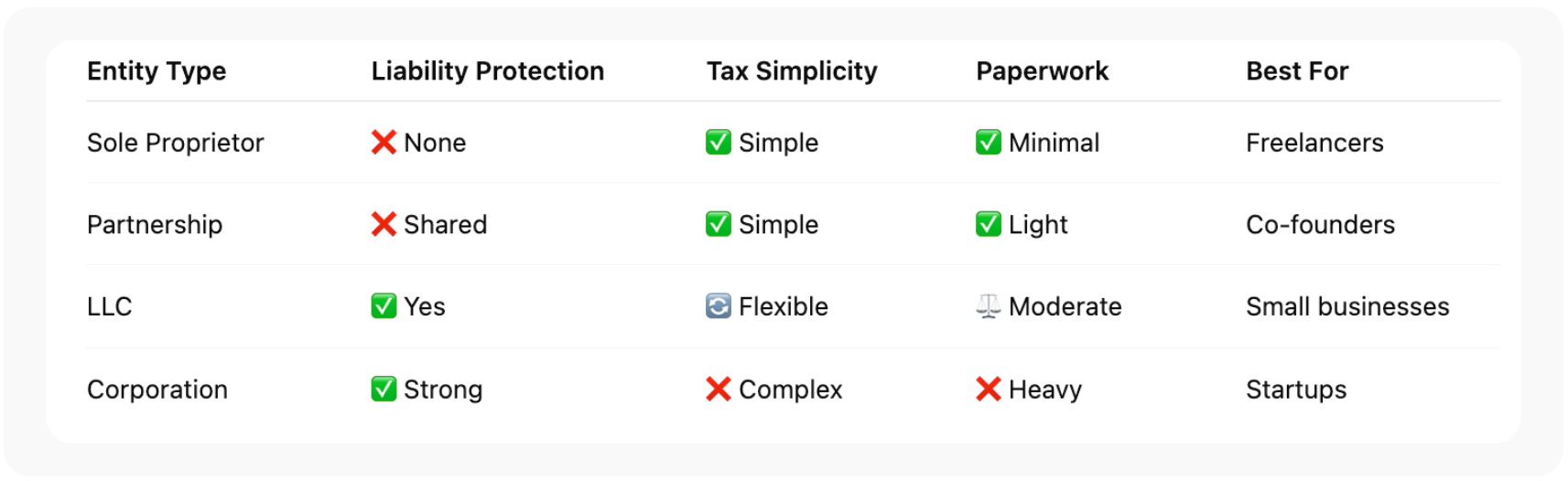

The Four Most Common Types of Business Entities

There are more than four types technically, but most businesses in the U.S. fall into one of these four. Let’s break them down without the jargon.

1. Sole Proprietorship

Best for solo entrepreneurs starting small

This is the default structure if you start doing business and don’t register anything. It’s super simple—but that simplicity comes with some trade-offs.

Good stuff:

- Easy and cheap to start

- You’re in full control

- Business income is just your income—no separate taxes

What to watch out for:

- You’re personally liable for everything (yes, everything)

- It can look less “official” to banks or clients

- Can’t bring on co-owners without changing your structure

Best for: Freelancers, consultants, or anyone testing an idea before going all in.

2. Partnership

For when you’re building something with someone else

If you and a partner start a business together, you’re automatically a general partnership unless you file something different. That means shared ownership—and shared liability.

Pros:

- Easy to set up with minimal paperwork

- Tax simplicity (pass-through income to each partner)

- Shared workload and startup costs

Cons:

- If your partner messes up, you’re still liable

- Disagreements can get messy without a solid agreement

- Can be tough to attract outside funding

Tip: Always create a partnership agreement, even with friends or family.

3. LLC (Limited Liability Company)

Flexible and protective—great for small teams or solo founders

The LLC is one of the most popular business entity types in the U.S. It offers a sweet spot: protection from personal liability, flexible tax services, and a fairly simple setup.

Why do people like it?

- Keeps your assets safe

- You can be taxed as a sole prop, partnership, or even an S corp

- Fewer formalities than in a corporation

- Works well for solo founders or small teams

Things to keep in mind:

- You’ll pay some formation and annual fees (depending on your state)

- Self-employment taxes may still apply

- More paperwork than a sole prop, but less than a corporation

So, what type of entity is an LLC?

It’s a hybrid. It borrows liability protection from corporations and tax flexibility from sole props and partnerships. That’s why it’s a common choice for small business entities.

4. Corporation (C Corp and S Corp)

Structured, scalable, and often used for start-ups

A corporation is a more complex legal structure designed for growth. There are two main types: C Corps and S Corps, each with its own rules.

C Corporation

- Separate legal entity (which means double taxation: once on profits, once on shareholder dividends)

- No restrictions on shareholders

- Ideal for businesses raising venture capital or planning to go public

S Corporation

- Pass-through taxation (no double tax)

- Limits on the number and type of shareholders

- Owners must pay themselves “reasonable compensation”

Overall Benefits:

- Strong liability protection

- Preferred by investors

- A clear structure for growth

Drawbacks:

- More paperwork and higher costs

- Formal requirements (like annual meetings and bylaws)

- Complex tax rules

Best for: Fast-growth start-ups, businesses raising capital, or anyone planning to bring in shareholders

What’s the Simplest Business Entity?

That would be the sole proprietorship. No forms to file, no fees to pay (in most states), and your business income just gets added to your tax return.

It’s simple—but simplicity can come at a cost. Mainly, you’re fully on the hook for everything your business does. If that makes you nervous, an LLC is probably worth considering.

So, What’s the Best Entity for a Small Business?

There’s no one-size-fits-all answer. But here’s a quick guide based on common goals:

| Goal | Consider This |

| Keep it simple, test an idea | Sole Proprietorship |

| Going in with a partner | Partnership or LLC |

| Want protection without a ton of rules | LLC |

| Planning to scale or raise money | Corporation (C Corp or S Corp) |

The best entity for a small business depends on your risk tolerance, tax situation, and how you plan to grow.

Let’s Talk About Liability

One of the biggest reasons to form an LLC or Corporation is liability protection. That means if your business is sued or falls into debt, your assets (like your house or car) are usually protected.

That’s not the case with a sole proprietorship or general partnership. It’s worth thinking about, especially if you’re signing contracts, handling client data, or selling physical products.

Also Read: Tax Liability And How You Can Calculate It

Orbit Accountants Can Help You Choose

We work with small business owners across the U.S. every day—freelancers, online store owners, consultants, creators, contractors, and more. One of the first questions we help answer is:

“What type of entity should I register?”

We don’t just give you a default answer. We look at:

- Your revenue goals

- Your tax situation

- Your risk exposure

- Where you’re doing business

- Where do you want to take this

Then we help you form it, file it, and stay compliant.

Not sure where to start? Talk to us now. It’s free, and you’ll walk away with clarity.

Conclusion

Choosing a business entity type isn’t just paperwork—it’s strategy. It affects your taxes, liability, and how future-ready your business is. If you get it right from the start, everything else gets easier.

Orbit Accountants can guide you through the process, break it all down without the legalese, and help you build a structure that fits your business now and later.

Ready to get it right? Book your consultation. We’ll help you figure it out- step by step.

Frequently Asked Questions:

What are the four types of business entities?

The main types of business entities are sole proprietorship, partnership, LLC (Limited Liability Company), and corporation. A corporation can be either a C Corporation or an S Corporation. Each type has its own rules for taxes, ownership, and legal protection.

What type of entity is an LLC?

An LLC is a business structure that gives you personal asset protection like a corporation but with simpler rules and flexible tax options. It’s often chosen by small business owners because it’s easy to manage and protects their savings or property if the business faces any legal or financial issues.

What is the best entity for a small business?

There’s no single best option—it depends on your business goals. Many small business owners go for an LLC because it offers both protection and flexibility. But if you’re running something very small, a sole proprietorship might work better. Some businesses also benefit from being an S Corporation, especially for tax reasons.

What is a small business entity?

A small business entity is a legal structure used for running a small business. It could be a sole proprietorship, partnership, LLC, or S Corporation. These setups are usually easier and cheaper to form and manage than big corporations.

What is the simplest business entity?

The simplest type is a sole proprietorship. It’s just one person running the business, and you don’t need to file separate taxes for it. There’s very little paperwork, and it’s quick to set up. But it doesn’t offer personal liability protection like an LLC or corporation does.

Disclaimer: This article is for informational purposes only and does not constitute legal or tax advice. Always consult with a qualified advisor before making business structure decisions.