Tax season can be a headache, especially when you’re left scratching your head about how to calculate your tax liability. The pressure of getting everything right can be overwhelming. After you start earning an appropriate amount regularly, paying taxes is something you can’t run from. And that is exactly why getting a grip on your tax liability is the key to succeeding and not getting any unexpected calls.

Let us try to understand this with these simple steps to calculate your tax liability and practical tips to keep things smooth sailing.

Table of Contents

What Is Tax Liability?

Tax liability meaning is the amount of tax you owe to the government. It refers to the total taxable amount you are legally entitled to pay, based on your income, assets, and any available deductions or credits.

So, What are Tax liabilities?

Well, It is the amount you need to pay after accounting for:

- Gross income (total earnings)

- Tax deductions (specific expenses that reduce taxable income)

- Tax credits (direct reductions in the amount of tax you owe)

Are you confident your business tax filings are fully optimized and compliant?

How To Calculate Your Tax Liability?

Understanding “what are tax liabilities” is more than just knowing how much is due. It is a way that helps someone make more rational financial decisions and avoid the underpayment of tax. Keeping up with their tax throughout the year prevents any underpayment penalties.

Though the process of “how to calculate your tax liability” can look exhausting it is quite easy if you know the steps.

Here’s what they are!

1. Determine Your Gross Income

This is your total income before deductions. It includes wages, business and rental income, and investment earnings.

2. Adjust Your Income

Subtract above-the-line deductions (adjustments). These can include contributions to retirement accounts, student loan interest, and HSA (Health Savings Account) contributions. The result is your Adjusted Gross Income (AGI).

3. Apply Deductions

Next, reduce your AGI by applying deductions. You can either:

- Take the standard deduction (a fixed amount based on your filing status: single, married filing jointly, etc.).

- Or, opt for itemized deductions, which allow you to deduct specific expenses like medical costs, mortgage interest, or charitable donations.

4. Use Federal Income Tax Brackets

The remaining income (taxable income) is subject to figuring federal income tax brackets. Different portions of your income are taxed at different rates, depending on the brackets you fall into.

5. Account for Tax Credits

Unlike deductions, tax credits directly reduce your tax bill dollar for dollar. Common credits include:

- Child Tax Credit

- Earned Income Tax Credit

- Education Credits (like the American Opportunity Credit)

6. Add Other Taxes

Depending on your situation, you might owe additional taxes, such as:

- Self-employment tax (if you’re self-employed).

- Net investment income tax (for high earners with investment income).

7. Subtract Withholdings and Payments

Finally, reduce your tax liability meaning by the taxes already withheld from your payroll management or any estimated payments you’ve made during the year.

Tips For You: Keep track of these calculations by using an online tax calculator or consulting a professional to avoid errors.

Explore Our Tools: Tax Deductions Calculator

How To Calculate Federal Income Tax Rate?

Figuring federal income tax rate is the rate at which your income is taxed. Understanding your tax rate can help you plan and make better decisions for your finances.

Here’s a simplified way to figuring federal income tax rate:

- Calculate Your Tax Liability: This is the amount of tax you owe after deductions and credits.

- Divide by Your Total Income: Take your tax liability and divide it by your total income. This gives you your effective tax rate.

Formula: Federal Income Tax Rate= (taxes owed/annual income) *100

For example, if you owe $5,000 in taxes and earn $50,000 annually, your effective tax rate would be 10%.

Did You Know?

The standard deduction for a single filer in 2023 was $13,850, and for married couples filing jointly, it was $27,700. This significantly reduced taxable income!

Types of Tax Liability

Tax liability meaning refers to the total amount of tax owed, which can come in various forms.

Here’s a breakdown of the most common types of tax liability for U.S. taxpayers:

- Income Tax

Income tax is a tax on your earnings, whether it’s from a job, business, or freelance work. The IRS calculates this tax based on your taxable income and the tax bracket you fall under. For example, if you earn $100,000 in a year, your tax liability will be based on the tax rates for that income range (e.g., 22% or 24% depending on the year).

- Sales Tax

Sales tax is applied to purchases of goods and services. It’s typically added at the point of sale. The rate varies depending on the state and locality. For instance, if you purchase an item for $500 in a state with a 7% sales tax, the total tax would be $35.

- Capital Gains Tax

This tax is applied to profits from the sale of assets like stocks, bonds, or real estate. For example, if you sell a house for $500,000 after purchasing it for $400,000, the $100,000 profit is subject to capital gains tax, which can vary depending on how long you hold the asset.

- Property Tax

Property tax is paid by homeowners based on the assessed value of their property. This is an ongoing tax paid to local governments (city or county). For example, if your home is valued at $250,000 and the property tax rate is 1.2%, your annual property tax liability would be $3,000.

- Corporate Tax

Corporations are required to pay taxes on their profits. The corporate tax rate varies based on business size and other factors, but for C-corporations, it’s a flat rate of 21% as of 2023.

- Self-Employment Tax

For freelancers, independent contractors, and business owners, self-employment tax includes Social Security and Medicare taxes. If you’re self-employed and make $50,000, your self-employment tax will be calculated based on a percentage of that income (around 15.3%, covering both Social Security and Medicare contributions).

If you’re feeling overwhelmed, it might be helpful to consult a tax professional or use a trusted online tool for guidance. It’s worth the investment to make sure you’re on the right track.

Also Read: What Does a Tax Advisor Do and How to Choose the Right One?

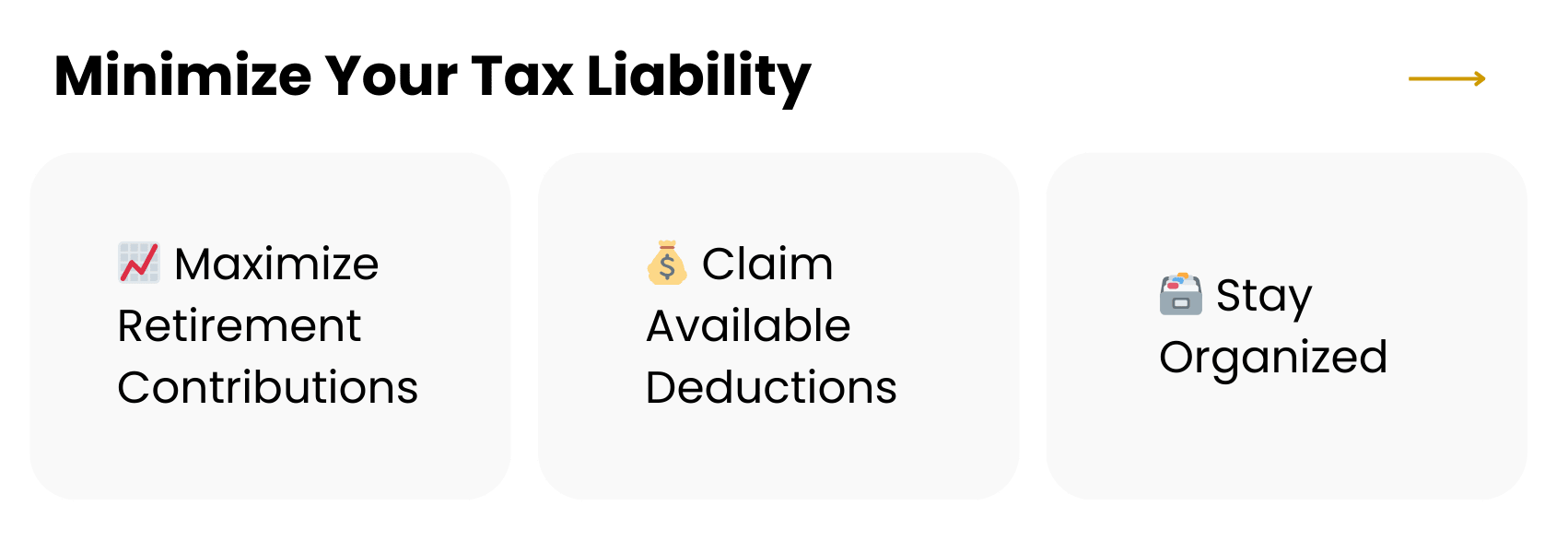

Tips To Minimize Your Tax Liability

There are a few methods to reduce tax liability including deductions, credits, and proper planning. Below are some to mull over:

- Maximize Retirement Contributions: Retirement account contributions to items like 401(k)s or IRAs lower your income tax and help you save for the future.

- Claim Available Deductions: Utilize every possibility presented to you with an item that lies under the standard and itemized deductions and grant credits for things like the Child Tax Credit.

- Stay Organized: Be sure to follow the record of all your incomes, expenses, and entropy regarding eligible deductions to seize everything when you file your reports.

Tips For You: Schedule quarterly reviews of your financial situation to avoid year-end shocks. Planning helps reduce the chance of errors and boosts your tax-saving opportunities.

Ready to Tackle Your Taxes?

Knowing the basics of tax liability and how to calculate federal income tax rates will help you be in charge of your future. Understanding tax liability is of prime importance in monitoring finances regardless of whether you plan to do your taxes on your own or hire a professional.

Do not hesitate to consult a tax expert from Orbit Accountants when you have any inquiries. You are not alone; a little help is just a click away!

Frequently Asked Questions:

Q. do I calculate my tax liability?

To calculate your tax liability, identify your total income from all sources, subtract eligible exemptions and deductions, and then apply the applicable tax rates. Finally, add any surcharges and cess to determine your total tax liability.

Q. What are the components that make up tax liability?

Tax liability includes your taxable income, the applicable tax rate based on income slabs, surcharges for higher income brackets, and cess (a fixed percentage added to the tax amount).

Q. How can I reduce my tax liability through deductions?

You can reduce your tax liability by claiming deductions under various sections, such as Section 80C (investments like PPF and ELSS), Section 80D (health insurance), and Section 24 (home loan interest), among others.

Q . What is the difference between tax liability and taxable income?

Taxable income is your income after deducting exemptions and deductions. Tax liability is the total amount of tax you owe, calculated by applying tax rates, surcharges, and cess to your taxable income.

Q. How can I estimate my tax liability for the year?

You can estimate your tax liability by calculating your expected income, deducting exemptions and deductions, and applying the tax rates and slabs. Online tax calculators can also help provide an accurate estimate.