A profit or loss statement (often called a P&L statement) is a core financial report that shows how much money your business made or lost over a set period. By listing total revenue, subtracting the cost of goods sold, and then accounting for various operating expenses, you see whether you’re turning a profit or facing a loss. Although the concept sounds straightforward, many business owners find themselves confused by the details—like which line items to include or how often to prepare a statement.

This article aims to simplify those points, offering practical insights and even a sample profit and loss statement template for your monthly, quarterly, or yearly needs.

Table of Contents

Introduction: Why a Profit or Loss Statement Matters

Among all financial reports, the profit and loss statement is one of the most crucial. Also known as a statement of profit, statement of operations, or simply a P&L, it helps you assess the financial performance of your business over a specific period of time. This timeframe might be a month, a quarter, or a year. By comparing revenue and expenses, you see if you’re generating net income or facing a shortfall.

Benefits of Regular P&Ls

- Insight into Profitability: Is your pricing strategy strong enough? Are your costs too high? A P&L clarifies these questions.

- Better Decision-Making: If your monthly profit and loss statement shows a dip in net income, you can respond quickly by cutting unnecessary expenses or driving up sales.

- Credibility with Stakeholders: Lenders or investors often want to see these statements to check that you’re financially stable. Even potential partners or suppliers might want evidence of consistent performance.

If you’re a small-business owner, ignoring the profit or loss statement can leave you in the dark. By staying updated, you not only handle day-to-day finances better but also plan for long-term sustainability.

Key Components of a P&L Statement

Most standard P&L statements (or profit and loss p&l) share similar line items, though the exact format can vary. Here’s a brief run-down:

- Revenue (Sales)

- This is the total money you brought in from selling products or services during the period. It might be split into categories if you offer different lines or want more detail.

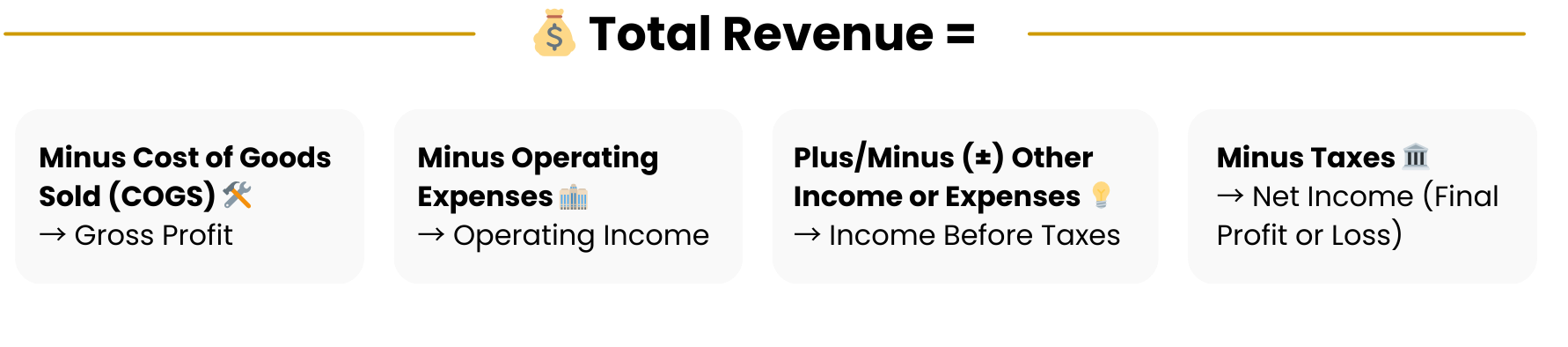

- Cost of Goods Sold (COGS)

- These are direct costs, such as raw materials, manufacturing labour, or wholesale costs. Subtracting COGS from revenue gives you “gross profit,” indicating how well you handle direct production costs.

- Operating Expenses

- Expenses not tied to manufacturing a specific product but essential for running the business. Examples: rent, utilities, marketing, salaries, insurance, office supplies. Subtracting these from gross profit yields “operating income.”

- Other Income or Expenses

- Might include interest income, gains or losses on asset sales, interest expense, or other items not part of everyday operations. Subtract or add these to get “income before taxes.”

- Taxes

- The portion you owe in taxes for that period. Subtracting it leads to the final net income or net loss figure.

Why Each Item Matters

- Revenue: Shows your top-line growth or decline.

- COGS: If it’s too large, your margin shrinks, leaving less to pay overhead.

- Operating Expenses: Where you might do cost-cutting if net income is down.

- Net Income: The bottom line, telling you if you’re profitable after all costs, including taxes and interest.

Setting Up Your Statement: Step by Step

Let’s walk through how to prepare a straightforward monthly profit and loss statement from scratch:

Step 1: Gather Revenue Data

Add up all sales from invoices, point-of-sale systems, or your e-commerce platform for that month. Ensure you separate refunds or discounts from your total revenue.

Step 2: Calculate Cost of Goods Sold

Sum direct costs: raw materials, any labour specifically for producing goods, or product purchase if you’re a retailer. This total is your cost of goods sold. Subtract it from revenue to find “gross profit.”

Step 3: List Operating Expenses

Group overhead items under logical categories—such as marketing, salaries, rent, utilities, travel—and add them up. Subtract from gross profit for your “operating income.”

Step 4: Add or Subtract Other Items

If you earned interest on a business savings account or had a one-time loss from disposing equipment, factor that in here. This step leads to income before taxes.

Step 5: Account for Taxes

If relevant for the period, subtract the estimated tax expense. The remainder is “net income.”

Step 6: Present the Final Figures

Your statement might look like:

- Revenue: $X

- COGS: $Y

- Gross Profit: $X – $Y

- Operating Expenses: $Z

- Operating Income: $(X – Y – Z)

- Other Items: +/- $A

- Income Before Taxes: $(X – Y – Z ± A)

- Taxes: $B

- Net Income: $((X – Y – Z ± A) – B)

This formula is universal, and you can adapt it whether you’re a solo freelancer or a growing enterprise.

Using Templates: Monthly Profit and Loss Statement Examples

Templates can be huge time-savers if you’re not sure how to lay out each line. You might find them in accounting software or from online resources. A typical monthly P&L template might include:

- Date or Period: e.g., “Month Ending June 30, 2025”

- Rows: (Revenue, COGS, Expenses, etc.)

- Columns: Actual amounts, possibly columns for comparisons to last month or last year

Key Template Variations

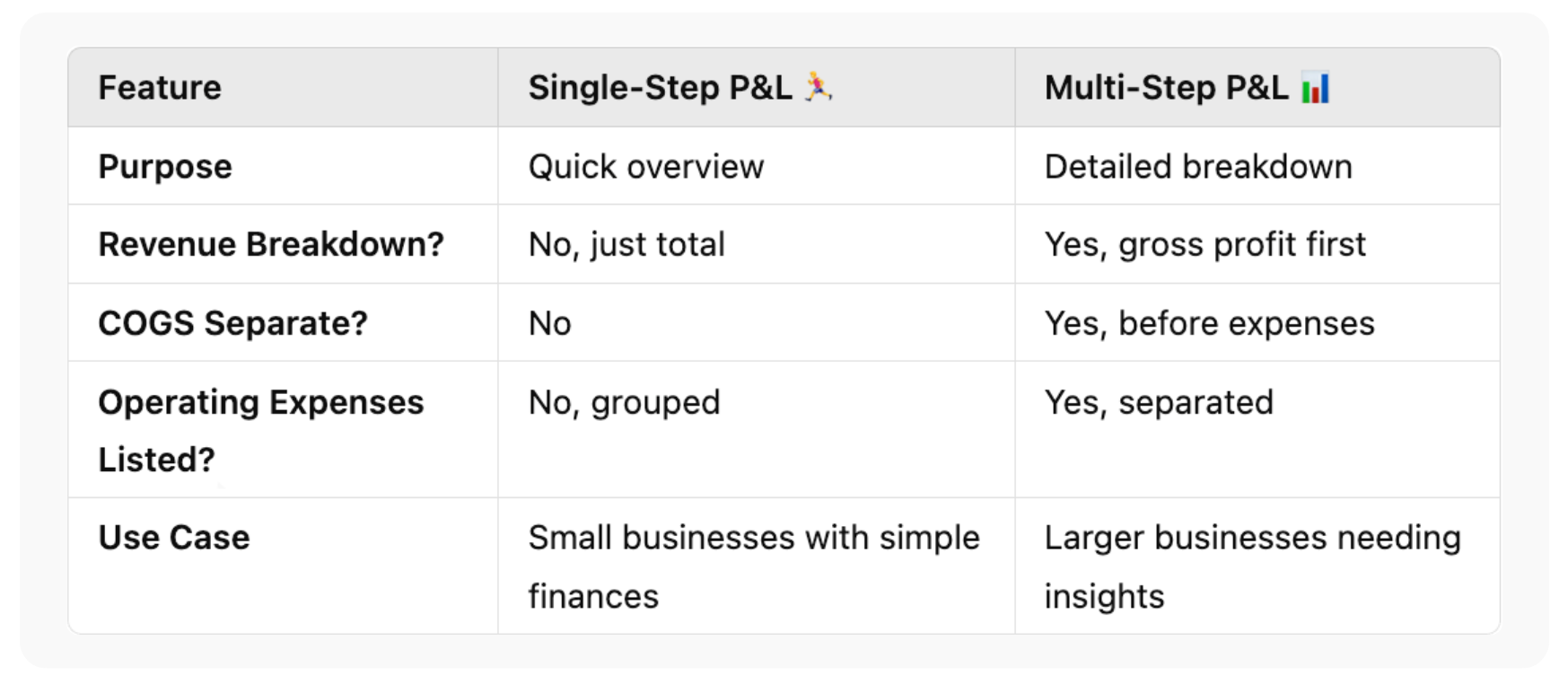

- Single-Step P&L: Summarizes revenue in one line, expenses in another, then net income. Simple but lacks detail.

- Multi-Step P&L: Breaks out gross profit, then subtracts operating expenses, then interest or taxes. This approach is standard for clarity.

How to Choose

If you only want a quick overview, single-step might suffice. If you prefer deeper insight—for example, to see if your direct costs soared or overhead ballooned—multi-step is better. Many small businesses adopt a multi-step monthly format because it reveals exactly where money flows.

Analyzing Results to Improve Financial Health

What’s the point of making a P&L if you’re not using it to guide decisions? After all, reading the statement should spur action.

Spot Patterns

Compare your monthly P&L across several months. If net income is steadily shrinking, track the cause. Has cost of goods sold jumped? Are you adding new employees without a matching revenue boost?

Evaluate Pricing

If your gross profit margin (Revenue – COGS / Revenue) is low, maybe your prices aren’t covering direct costs well. Or your overhead might be too high, leaving insufficient net profit.

Consider Overhead Adjustments

Operating expenses might be out of control. High marketing spend can be fine if it yields strong revenue growth. But if it doesn’t, a P&L highlights the mismatch.

Plan for Tax Season

A monthly profit or loss statement ensures no surprises come tax time. If your net income is consistently high, set aside funds for taxes. If you see a loss, you might adjust your spending or consider deferring expansions until your finances stabilize.

Cash Flow Link

Although P&L statements differ from the cash flow statement, a healthy net income generally leads to better cash positions—unless your accounts receivable are delayed. If your P&L is strong but your bank account is empty, it might be time to improve your collections process or re-check your payment terms.

Common Pitfalls and How to Avoid Them

1. Mixing Personal and Business

When owners commingle personal spending with business, the P&L becomes murky. Keep a separate business account to ensure clarity.

2. Forgetting to Record All Expenses

Some skip small items (like office supplies or monthly software fees), assuming they’re too small to matter. Over time, these add up and distort your net income.

3. Neglecting Depreciation or Amortization

If you buy big-ticket equipment, you might spread out its cost via depreciation. Missing these can overstate net profit in the early stages.

4. Overcomplicating the Template

Too many micro categories can bury you in detail. Stick to a structure that’s simple enough to maintain but detailed enough to give real insights.

5. Failing to Revisit

Updating the statement yearly is too infrequent, especially in a volatile market. Monthly or at least quarterly updates help you spot trends quickly.

Frequently Asked Questions:

1. How do I create a monthly profit and loss statement for my business?

First, gather monthly revenue and group them as total sales. Next, list cost of goods sold to find gross profit. Subtract overhead expenses (rent, marketing, wages) to get operating income. Then account for interest or taxes, leaving net income. You can use spreadsheet templates or accounting software for simplicity.

2. How does a profit or loss statement help with financial planning?

By revealing where money flows—like direct costs vs. overhead vs. taxes—you see if you have enough leftover to invest or expand. It also ensures you detect cost spikes early, so you can pivot quickly rather than learning too late.

3. What is the purpose of analyzing a monthly profit and loss statement?

It’s about real-time insight. Monthly statements let you see if your decisions (like a new marketing campaign) are boosting net income or if new expenses overshadow your gains. This frequency prevents major financial drift.

4. How often should I update my profit or loss statement?

Monthly is ideal for dynamic businesses. Quarterly can work if your model is more stable. Yearly is common for official tax records, but it’s too long to wait for day-to-day management.

Conclusion and Next Steps

Whether you call it a profit or loss statement, p and l statement, or statement of operations, the bottom line is the same: you want to see if you’re making money or not. This crucial financial report helps you track revenue, weigh it against direct and indirect costs, and see your net income. By comparing months or quarters, you spot trends—like if your product margins are improving or if overhead is climbing too fast.

Next Steps

- Adopt a Template: If you haven’t already, pick a consistent monthly profit and loss statement template. Simple or multi-step depends on your detail needs.

- Record Diligently: Don’t skip small bills or minor revenue streams. They can shift your net profit.

- Review: Each month, see if net income meets your goals. If it’s below target, do you need to raise prices or cut certain expenses?

- Integrate: Link your P&L analysis to other statements like cash flow. A P&L might say you’re profitable, but if you’re not collecting on invoices quickly, your bank account might still run low.

- Stay Curious: Keep reading about best practices, whether for inventory management, overhead reduction, or tax strategies. The more you understand, the more effectively you’ll shape your business’s future.

With a better handle on profit and loss statements, you’ll find yourself making smarter decisions—like identifying which product lines truly shine, or adjusting your marketing spend if it’s not yielding enough return. Ultimately, that’s the real purpose of the P&L: not just a formality for the year-end but a tool for guiding your daily and strategic moves toward stable growth.