Table of Contents

What Is a Balance Sheet?

A balance sheet is a financial statement that shows a snapshot of a company’s financial position at a specific point in time. It lists the business’s assets, liabilities, and equity. Simply put, it answers: what does the business own, what does it owe, and what’s left for the owner?

It follows a simple rule known as the accounting equation:

Assets = Liabilities + Equity

This equation is the backbone of every balance sheet, ensuring everything stays in balance. A properly prepared balance sheet offers insight into the company’s financial position, providing the clarity needed to manage growth, anticipate cash flow issues, and assess the impact of key financial decisions.

Are you confident your business tax filings are fully optimized and compliant?

Why Balance Sheets Matter for Small Businesses?

For small business owners, the balance sheet is more than a compliance tool—it’s a roadmap. It helps:

- Track what you own and owe

- Show lenders or investors your financial health

- Make informed growth or borrowing decisions

- Stay aligned with financial goals

Whether you’re buying equipment, hiring staff, or securing a loan, having your statement of financial position in order is crucial. A solid balance statement sample also boosts credibility, demonstrating that you operate with transparency and financial discipline. This is especially important when applying for grants, attracting partners, or preparing for audits.

Key Components of a Balance Sheet

Here are the three major sections you’ll always see:

Assets

Assets include everything your company owns with value:

- Cash and cash equivalents (liquid assets, like bank balances)

- Accounts receivable (customer payments due)

- Inventory (goods for sale)

- Fixed assets (like equipment, buildings, vehicles)

- Long-term assets (e.g., investments, trademarks)

Assets include both tangible and intangible items and are typically listed in order of liquidity.

Liabilities

These are debts and obligations:

- Accounts payable (vendor bills)

- Credit card debt

- Short-term loans (due within a year)

- Long-term liabilities like mortgages or business loans

- Deferred revenue (prepaid customer orders)

Keeping an eye on long-term debt and borrowing money obligations helps you manage risk and plan for future payments.

Equity

This represents the owner’s stake in the company:

- Retained earnings (cumulative profits not paid out)

- Owner’s equity (investment by the business owner)

- Common stock (for corporations)

Understanding the balance of assets, liabilities, and equity allows you to measure your financial position balance sheet with confidence.

Understanding the Accounting Equation

Let’s revisit this fundamental formula:

Assets = Liabilities + Equity

Every transaction in your business impacts this equation. It must always stay balanced, or something’s off in your records.

Example: If you borrow $10,000 to buy equipment, your assets increase by $10,000 (equipment), and liabilities increase by $10,000 (loan).

This is the foundation of double-entry bookkeeping, ensuring every balance sheet sample remains accurate. It also reinforces the connection between operational activity and financial structure.

Sample Balance Sheet Template Explained

Here’s a basic balance sheet example for a small business:

| Assets | Liabilities & Equity | ||

| Cash | $5,000 | Accounts Payable | $3,000 |

| Accounts Receivable | $2,500 | Credit Card Debt | $1,000 |

| Inventory | $7,000 | Long-Term Debt | $5,000 |

| Equipment | $10,000 | Total Liabilities | $9,000 |

| Total Assets | $24,500 | Owner’s Equity | $15,500 |

| Total Liab. + Equity | $24,500 |

This accounting sheet example shows how assets on the left side align with liabilities and equity on the right. It’s also useful for comparing month-over-month or year-over-year changes, spotting shifts in liquidity, and refining capital strategies.

Common Line Items and Their Meaning

- Accounts Payable: Bills you owe vendors for supplies or services.

- Cash and Cash Equivalents: Your available cash or bank funds.

- Retained Earnings: Accumulated profit that has been reinvested.

- Long-Term Liabilities: Debt with maturity beyond one year.

- Fixed Assets: Long-term resources used in operations (e.g., machinery, property).

Grasping the components of meaning behind these terms helps you go beyond the numbers and understand how they shape your strategy. For instance, rising accounts payable might indicate better vendor terms—or potential cash flow trouble if unmanaged.

Life Out of Balance: What Your Sheet Might Be Telling You

When your balance sheet isn’t balancing, it’s a red flag. Here’s what might be wrong:

- Data entry errors: Numbers entered in the wrong column

- Miscalculated totals: One side doesn’t add up

- Missing transactions: A forgotten invoice or bank charge

- Trial balance mismatches: Input errors in your source data

Experiencing a “life out of balance” moment might indicate deeper systemic issues—like outdated systems or lack of financial oversight. Regularly reconciling your books and using generally accepted accounting principles (GAAP) can help avoid these situations.

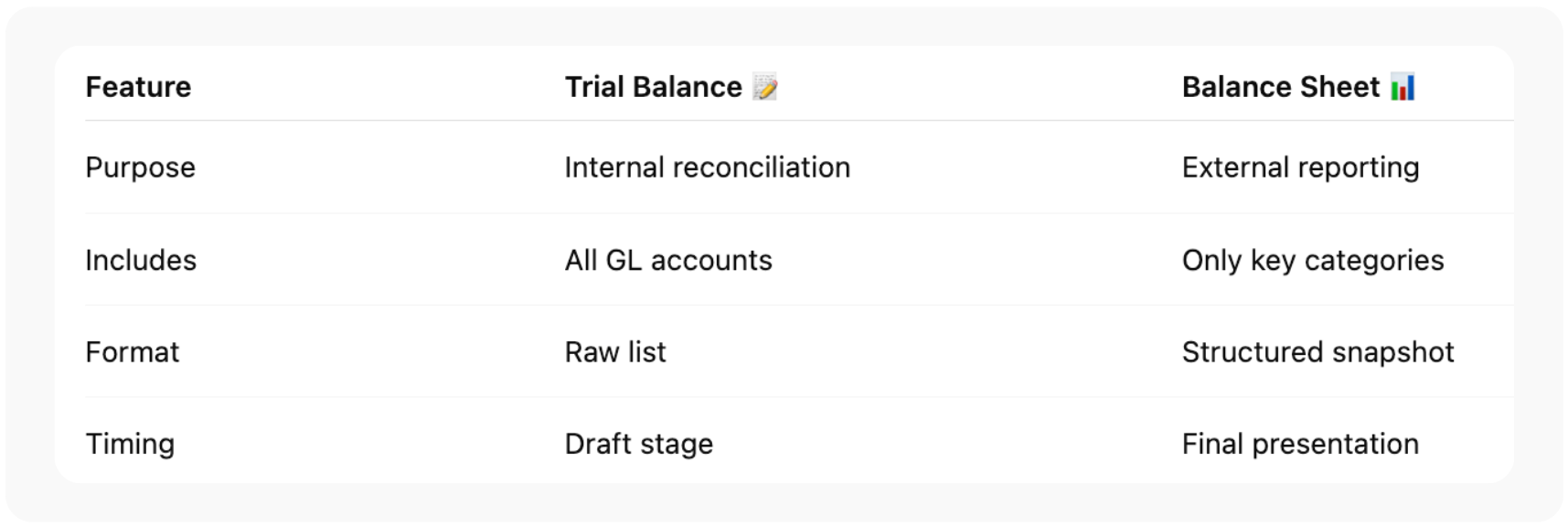

Balance Sheet vs. Trial Balance: Key Differences

The trial balance of balances is a comprehensive list of all general ledger accounts and their closing balances. It’s primarily used for internal bookkeeping.

A balance sheet, however, filters relevant accounts to present a structured summary of your financial position. It’s intended for stakeholders, such as lenders, investors, or the IRS.

Trial Balance = Draft working document Balance Sheet = Final financial snapshot

Understanding both helps ensure your records flow logically into your formal statement of financial reports.

How to Read a Company’s Financial Position Like a Pro?

Want to assess a company’s health? Here’s where to look:

- Check cash reserves: Ample cash and cash equivalents offer safety nets.

- Evaluate liabilities: High long-term liabilities might pose repayment risks.

- Analyze equity trends: Are retained earnings rising or dipping?

- Compare total assets and liabilities: A widening gap suggests strength; a shrinking one indicates potential debt issues.

Reading a company’s balance sheet effectively helps uncover trends, hidden risks, and opportunities for better financial management.

Tools & Software to Simplify Balance Sheet Prep

Gone are the days of creating balance sheets in Excel manually. Today’s accounting software can:

- Auto-populate reports from transactions

- Generate customizable balance sheet layouts

- Track performance by month, quarter, or year

- Sync with bank accounts, payroll, and billing tools

Popular options like QuickBooks, Xero, Zoho Books, and Wave are especially useful for small business owners. They provide intuitive dashboards, cloud-based access, and alignment with accepted accounting principles GAAP.

Final Takeaway: Using Balance Sheets to Make Smart Decisions

Your company’s balance sheet isn’t just about reporting—it’s a decision-making compass. Here’s how it helps:

- Borrowing money: Understand your debt capacity

- Strategic planning: Identify funding gaps or asset accumulation

- Budgeting: Adjust your plans based on actual figures

- Risk management: Catch imbalances early

A reliable balance statement sample helps you evaluate where your business stands—and where it can go.

Frequently Asked Questions:

What is a balance sheet used for?

A balance sheet provides a snapshot of a company’s financial health, showing assets, liabilities, and equity at a specific time.

What is included in a balance sheet?

Assets (like cash and equipment), liabilities (like debt), and owner’s equity (like retained earnings).

What is the difference between a balance sheet and income statement?

A balance sheet shows financial position at a point in time; an income statement shows financial performance over time.

Is a balance sheet required for all businesses?

It depends. While not mandatory for sole proprietors, it’s recommended for tracking your business health.

How often should I update my balance sheet?

Monthly or quarterly updates are common, especially for decision-making and lender reporting.