Accounting might not be the flashiest part of your business—but liabilities? They’re the part you can’t afford to ignore. But here’s the thing: if you’re a business owner in the US (or even just someone trying to get a handle on your finances), understanding liabilities in accounting is non-negotiable.

Why? Liabilities tell a pretty important story about your financial obligations, your current standing, and where you might be heading. Every strategic choice, from taking out a loan to growing your team, depends on how well you manage your liabilities.

So, let’s understand the basics, starting with the big question: what is liability in accounting?

Table of Contents

What is Liability in Accounting?

Alright, down to the brass tacks. So, what is liability in accounting?

In simple terms, a liability is something you owe. It’s a financial obligation your business has to pay at some point, whether that’s tomorrow or ten years from now. These can be things like loans, unpaid bills, or taxes.

On your balance sheet, liabilities are stacked alongside your assets and equity. They help paint a full picture of your financial position. Knowing your liabilities is critical if you want to make smart decisions, plan for the future, or even just avoid cash flow chaos.

Think of it like this: if assets are what your business owns, then liabilities are what it owes. And trust us—tracking both sides of that equation is essential for solid, accurate accounting.

So again, if someone ever asks you what liability is in accounting, you now know it’s all about those obligations your business is expected to settle.

Are you currently managing your bookkeeping in-house?

Types of Liabilities in Accounting

When we talk about liabilities in accounting, we’re not talking about just one kind of thing. There are a few categories, and each plays a different role in your financial life.

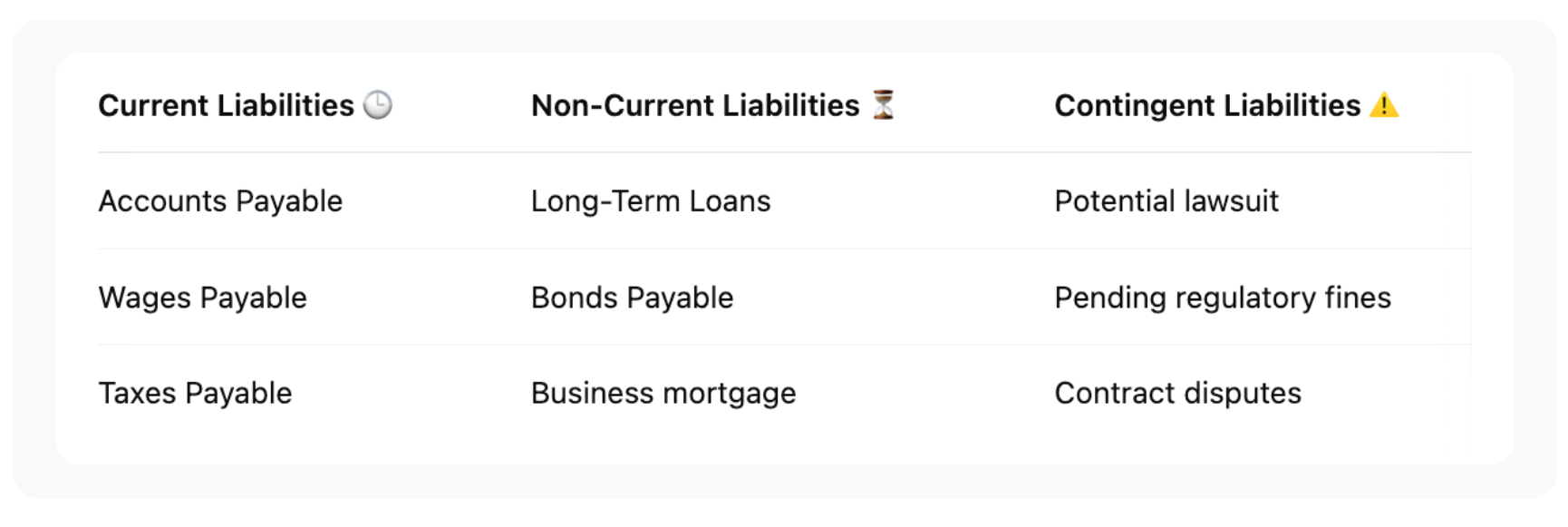

- Current Liabilities

These are the bills that are coming due soon—as in, within the next 12 months. Common examples include:- Accounts Payable – unpaid supplier invoices

- Wages Payable – what you owe your employees for work they’ve already done

- Short-Term Loans – like a credit line, you’ll be paying off in the next few months

- Taxes Payable – yes, the IRS wants its share

If it’s coming up soon and requires a payment, it’s probably a current liability.

- Non-Current Liabilities

These are your long-term obligations—think over a year out. Examples include:- Long-Term Loans – like your business mortgage or that 5-year SBA loan

- Bonds Payable – if your company has issued debt to raise capital

They might not be urgent, but they definitely aren’t to be forgotten. These can significantly impact your long-term strategy.

- Contingent Liabilities

These are the “maybe” kinds of liabilities. They depend on the outcome of a future event, like a lawsuit. If you get sued and lose, you’ll owe money. Until then, it’s just a potential obligation.

Tracking all types of liabilities in accounting—including contingent ones—is essential for getting a full and accurate picture of your company’s financial health.

Examples of Liabilities in Accounting

Let’s make this real. Here are a few examples of liabilities in accounting that pop up in almost every business, big or small:

- Accounts Payable: Got a stack of unpaid vendor invoices? That’s a liability. You’ve received the goods or services, but the bill’s still open.

- Salaries Payable: Your team has worked, but payday’s still a few days out. Until you cut those checks, that’s a liability.

- Taxes Payable: Uncle Sam doesn’t forget. Whether it’s sales tax, payroll management tax, or corporate income tax, it’s on your books until paid.

- Loans Payable: Maybe you took out a small business loan to upgrade equipment. Until it’s paid off, that debt is a liability.

- Unearned Revenue: Weird one, right? But if a customer pays in advance for a product or service you haven’t delivered yet, that money sits on your balance sheet as a liability—until you fulfill the promise.

Imagine a local gym that sells annual memberships. The upfront cash is great, but they technically owe their customers access for the next 12 months. That’s unearned revenue, and yes—it’s a liability.

These examples of liabilities in accounting show up in everyday business life, and staying on top of them helps you avoid financial surprises.

How do Liabilities Differ from Assets and Equity?

Here’s where things get a little more visual.

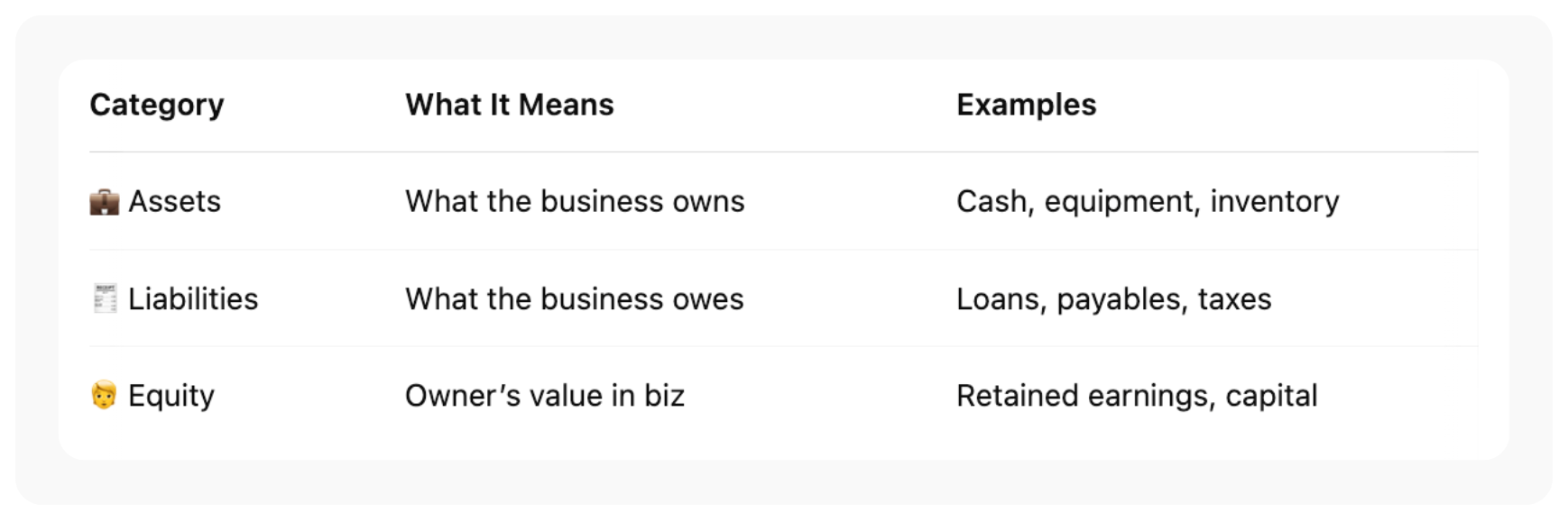

| Category | Definition | Example |

| Assets | What your business owns | Cash, inventory, equipment |

| Liabilities | What your business owes | Loans, accounts payable, taxes |

| Equity | The owner’s stake in the company | Retained earnings, capital investments |

They all tie together in the accounting equation:

Assets = Liabilities + Equity

This is the foundation of every balance sheet out there. Your liabilities don’t exist in isolation—they work hand in hand with assets and equity to show your business’s true financial picture.

Importance of Managing Liabilities Effectively

You wouldn’t ignore your bills at home (hopefully), and the same goes for your business. Managing liabilities in accounting is vital for a few key reasons:

- Cash Flow: If you’re not keeping up with what’s due you could find yourself short on cash when you need it.

- Creditworthiness: Lenders look at your liabilities when deciding whether to extend credit. A mountain of unpaid debt? Red flag.

- Financial Health: A well-balanced liability load shows you’re investing in your growth, but not drowning in debt.

Common Mistakes to Avoid

Some businesses fall into traps like:

- Forgetting to record liabilities that haven’t hit the bank account yet (like accrued wages).

- Treating unearned revenue as income too early.

- Not separating short-term and long-term liabilities.

Staying organized, using reliable accounting and bookkeeping tools, and keeping a clear record of what your business owes can help you stay on top of your finances. And honestly, having a good accountant makes it even easier.

Liabilities in Accounting: Key Takeaways for Small Businesses

Here’s a quick recap for small business owners:

- Always know what you owe and when it’s due.

- Don’t let short-term obligations sneak up on you.

- Make sure your balance sheet reflects reality.

- Track liabilities just as carefully as income or expenses.

Partnering with a professional can make this way easier. Orbit Accountants, for instance, specializes in helping small businesses understand their accounting liabilities, so you’re never caught off guard.

Conclusion

So, we’ve covered a lot—what is liability in accounting, the different types, examples of liabilities in accounting, and why all of it matters so much. The bottom line? If you want to make smart, sustainable financial decisions for your business in the US, understanding and managing liabilities is a must.

Don’t leave it to chance. Whether you’re trying to sort through current debts, plan for future obligations, or just make sense of your balance sheet, Orbit Accountants has your back.

Need help managing your business liabilities? Let’s get it sorted—reach out to Orbit Accountants today and take one more thing off your financial plate.

Frequently Asked Questions:

1. What is a liability in accounting in simple terms?

A liability is anything your business owes to someone else, like money owed to suppliers, upcoming loan payments, or taxes due. It’s a promise to pay in the future and shows up on your balance sheet as part of your company’s financial obligations.

2. What is the basic concept of liabilities?

Liabilities represent outside claims on your business’s assets. In other words, they’re the financial responsibilities your company has to others—things like bills, loans, or deferred revenue. Understanding your liabilities helps you track how much of your assets are spoken for.

3. What is the difference between debt and liabilities?

Debt is a specific type of liability, usually involving borrowed money, like a bank loan or a line of credit. Liabilities are the bigger picture and include all financial obligations, such as unpaid bills, wages owed, and even taxes. So, all debt is a liability, but not every liability is debt.

4. Are expenses liabilities or assets?

Expenses are neither; they’re in their category. Expenses are the costs of running your business, like rent or utilities. But if you haven’t paid an expense yet—say you owe rent—it temporarily becomes a liability until it’s paid.