& How It Works_")

If you’ve taken out a loan, used a credit card, or checked out mortgage offers, there’s a good chance you’ve seen the term APR. Most people do. But honestly, not everyone pauses to understand what it really means.

APR, short for Annual Percentage Rate, isn’t just another financial acronym. It plays a direct role in how much you’ll end up repaying when you borrow money. And not just the interest, it includes fees too. That’s why it matters more than most people realize.

This isn’t a crash course in finance, just a simplification of APR meaning, how it’s calculated, and how it affects your wallet. Let’s break it all down, below.

Table of Contents

APR Meaning: What Is Annual Percentage Rate?

So, what is APR, really?

Think of it as the full price tag on borrowed money, the total yearly cost including both the interest rate and extra charges like processing fees. This percentage helps you figure out exactly what you’re signing up for when you take out a loan or swipe your credit card.

Let’s say you Google “APR meaning” or “what is APR” ; here’s what it boils down as a difference APR and interest rate to:

APR = Interest + Fees, spread over a year.

It’s especially helpful when comparing financial products. Two offers might advertise the same interest rate, but their Annual Percentage Rates can be very different once fees come into play. APR gives you the big picture.

Would strategic financial oversight from a Fractional CFO add value to your operations?

How Does APR Work?

Wondering how does annual APR work in day-to-day situations?

Let’s use an example: You borrow $10,000 with a 10% interest rate. The lender also charges a $500 processing fee. Once those fees are factored in, your APR will likely be higher than 10%, because it reflects the true cost over a year.

Now, the formula lenders use can look a bit technical, but thankfully you won’t have to solve it yourself. Financial institutions are legally required to show the Annual Percentage Rate in your agreement, so you’re clear on what you’ll owe.

Knowing how APR works helps you:

- Compare loans from different lenders

- Understand hidden fees upfront

- Pick the option that costs you less in the long run

APR isn’t just a number, it’s a smart decision-making tool.

APR vs. Interest Rate: What’s the Difference?

It’s one of the most common questions: What’s the difference between APR and interest rate?

Both are percentages. Both relate to borrowing. But they aren’t the same.

Here’s the breakdown:

- The interest rate is just the cost of borrowing money.

- The APR includes that, plus other charges like application fees, closing costs, and annual card fees.

Example:

A personal loan might advertise a 7% interest rate, but with fees, the APR could come out to 8.2%.

Or a credit card might have a 16% interest rate, but once you add yearly charges, the Annual Percentage Rate becomes 21%.

When you’re comparing options, don’t just look at the interest. Look at the full APR meaning, it could save you more than you think.

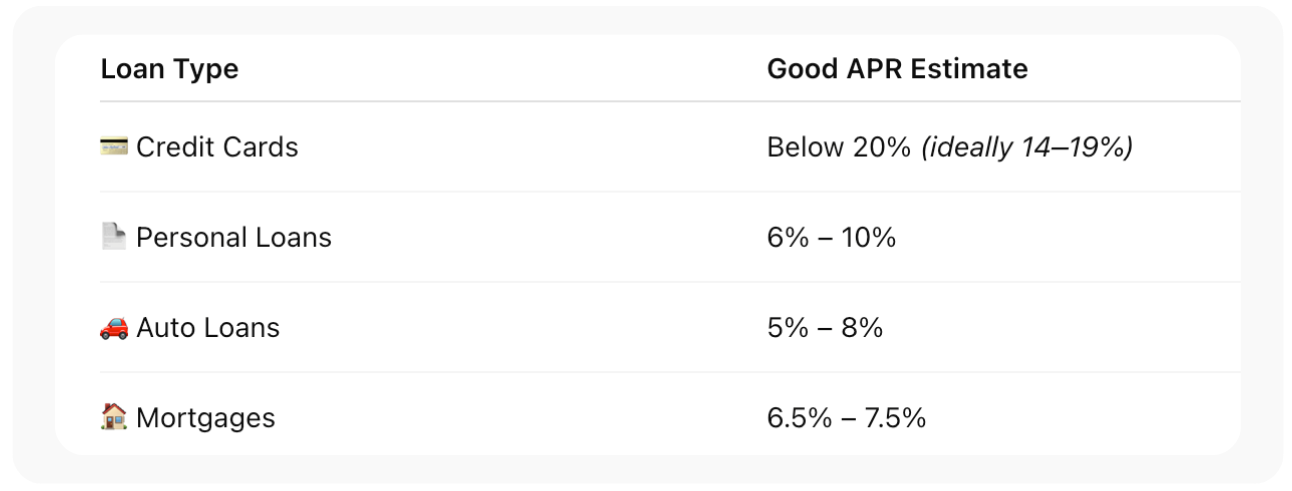

What Is a Good APR in Today’s Market?

So, what is a good APR right now?

It really depends on a few things; like what kind of loan you’re taking, your credit score, the market rate, and even the lender’s policies. That said, here’s a general idea of what counts as a good APR today:

If your APR falls within or below these ranges, you’re doing pretty well. But even with a strong credit profile, be cautious; some lenders may hide extra charges in the fine print that push your APR higher.

A good APR reflects more than numbers. It signals healthy credit habits and a low-risk borrower. Want better rates? Start by cleaning up your credit, paying bills on time, and reducing debt.

Why APR Is Important for Borrowers

Now let’s talk about why APR really matters.

Every loan and credit card comes with a cost. But APR tells you the total cost, not just what you pay monthly, but what you’ll pay over time.

With credit cards, APR kicks in when you carry a balance from one month to the next. Even a few days can trigger interest charges. For loans, a higher APR means you’ll pay more in the long run; even if your monthly payments seem manageable.

Knowing your APR meaning can be the difference between manageable debt and paying thousands extra over the years.

How to Keep Your APR Low

APR isn’t always fixed. There are smart ways to keep it in check, especially with credit cards and personal loans.

Here’s how to manage it:

1. Boost Your Credit Score

The better your score, the better your chances of getting a good APR. Pay bills on time, keep your credit usage low, and avoid unnecessary applications.

2. Compare Offers

Don’t take the first loan you’re offered. Shop around. Lenders compete, and that gives you options.

3. Ask for a Better Deal

If your financial situation has improved, ask your lender for a reduced rate or consider refinancing.

4. Watch Out for 0% APR Traps

Some credit cards offer 0% intro APR periods. Great for big purchases, but be careful. Once that window closes, regular APR applies.

5. Always Pay in Full

Avoiding APR on credit cards is simple: pay your balance in full before the due date. If you don’t carry a balance, there’s no interest to charge.

Conclusion

APR might look like just another number on your loan or credit card statement. But ignoring it can lead to paying a lot more than you should.

Understanding what APR means, how it’s different from the interest rate, and what a good APR looks like today can help you borrow smarter and save money. It’s not just about percentages, it’s about making better financial decisions.

Not sure how to compare APRs or choose the right option? Orbit Accountants is here to guide you. We make confusing terms simple and help both individuals and businesses make confident money moves.

👉 Book your free consultation today and get clear, personal advice that works for you.

Frequently Asked Questions

How does annual APR work?

APR represents the total yearly cost of borrowing. It includes both interest and lender fees, giving you a full picture of what you’ll pay over time.

Will I be charged APR if I pay in full?

If you pay your credit card bill in full every month and on time, you usually avoid APR charges on new purchases.

Why is my APR so high with good credit?

It might depend on the lender, loan type, or market conditions. Some cards with high rewards come with higher APRs. Always compare terms and consider switching if needed.

Can you avoid paying an APR?

Yes. Paying your credit card balance in full is the easiest way. For loans, it’s all about comparing offers and reading the terms carefully to avoid unnecessary fees.