Save up to 20% of your business income: Here’s how to benefit from the Qualified Business Income Deduction

If you own a business, as a one-person operation, LLC holder, or small team leader, you are always thinking about legal ways to cut down your tax bill. This is where the deduction for qualified business income (QBI) comes in. QBI is one of the most generous yet underutilized tax breaks available to small-business owners in the U.S.

Simply put, this deduction allows any eligible business owner to deduct up to 20% of his or her qualified business income from taxable income. This deduction could save a small business owner thousands, and this is without having to worry about itemizing the deductions, let alone jump through an overburden of hoops.

Let us explore how it works and how you can benefit from it.

Table of Contents

What Is Qualified Business Income (QBI)?

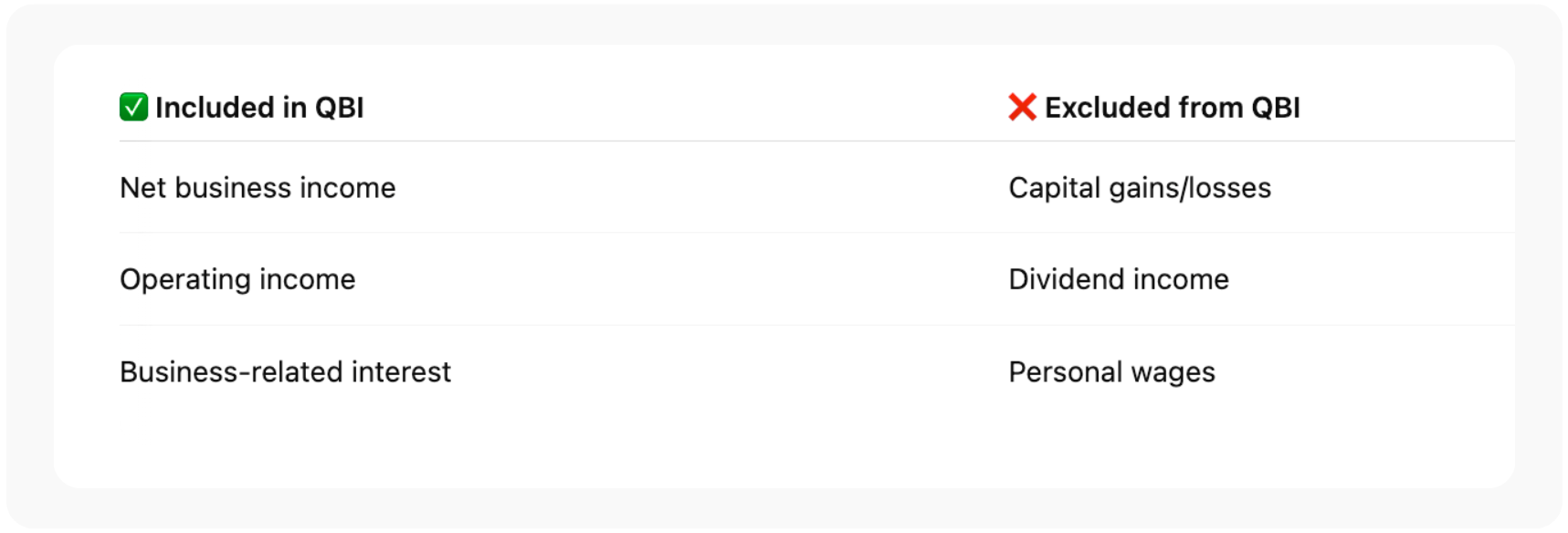

Qualified Business Income (QBI) refers to your business’s net income — after operating expenses, but before taxes. It excludes several types of income such as:

- Capital gains or losses

- Dividend income

- Interest income (unless it’s business-related)

- Wages paid to yourself

- Income earned outside your business

Example:

If you own a digital marketing agency and bring in $150,000 in revenue, with $50,000 in expenses, your QBI would be $100,000. You could deduct up to 20% of that if you qualify — saving $20,000 from your taxable income.

This deduction only applies to income from pass-through entities — businesses that pass their income directly to their owners’ tax returns. These include:

- Sole proprietorships

- Partnerships

- S corporations

- LLCs (treated as any of the above)

- Certain trusts and estates

Are you currently managing your bookkeeping in-house?

Who Qualifies for the QBI Deduction?

The qualified business income deduction is intended to benefit small and mid-sized business owners. Generally, if you’re self-employed or own a pass-through business and your total taxable income is below the IRS thresholds, you likely qualify.

For the 2024 tax year, the income limits are:

- $191,950 for single filers

- $383,900 for married couples filing jointly

If your taxable income is under these thresholds, you may be eligible for the full 20% deduction.

If your income exceeds these thresholds, you might still qualify — but with added limitations, depending on the nature of your business and your wage and property structure.

What Happens If You Earn Over the Threshold?

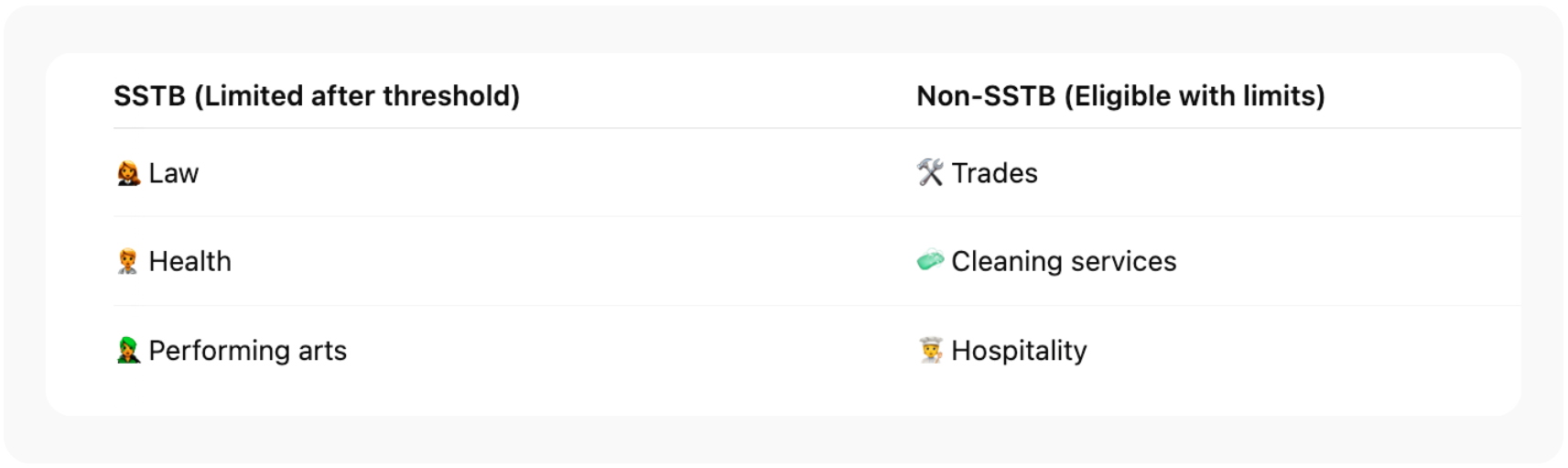

If your taxable income exceeds the IRS limits, the deduction for qualified business income calculation becomes more complex. The IRS will look at:

- Whether your business is a Specified Service Trade or Business (SSTB

- The amount your business pays in W-2 wages

- The unadjusted basis of qualified business property (UBIA)

SSTBs include professions in law, accounting, health, consulting, financial services, and performing arts. These businesses face a phase-out of the deduction as income increases beyond the thresholds.

If your business is not an SSTB, your deduction may still be limited based on:

50% of W-2 wages paid

or

25% of W-2 wages plus 2.5% of the original value of certain business property

The bottom line: if you’re over the income limit, you’ll need to run the numbers carefully — or have a tax expert do it for you.

How to Calculate the QBI Deduction?

The qualified business income deduction is the lesser of:

20% of your qualified business income

or

20% of your taxable income minus net capital gains

Example:

If your QBI is $80,000 and your taxable income is $100,000 (with no capital gains), you’d qualify for a deduction of $16,000.

| QBI | Taxable Income | Capital Gains | Deduction |

| $80,000 | $100,000 | $0 | $16,000 (20% of QBI) |

| $120,000 | $130,000 | $10,000 | $20,000 (20% of $100,000 taxable income minus capital gains) |

For higher earners, the W-2 wage and property formulas may further limit the deduction. If you have multiple businesses or investment-related income, the calculations can get even more complex — especially if one of your businesses is an SSTB.

Need help? The IRS has detailed instructions in Form 8995.

Which Taxes Does the QBI Deduction Reduce?

The deduction for qualified business income only reduces your federal taxable income. It does not reduce self-employment tax, Social Security, or Medicare taxes.

Still, the deduction can result in significant federal income tax savings, especially for individuals in higher tax brackets or those running profitable businesses.

Tips to Maximize Your QBI Deduction

- Maintain accurate income records – Understanding your taxable income and how close you are to the IRS thresholds can help you plan and adjust before tax season.

- Strategically pay wages – If you’re an S corp owner, balancing W-2 wages and distributions can impact how much of the deduction you qualify for.

- Invest in qualified property—For high-income earners, property ownership can help preserve their deduction through the 2.5% rule.

- Evaluate your entity structure – Choosing the right business structure can have a big impact on your eligibility and how the deduction is calculated.

- Work with a professional – The rules can be nuanced. A tax advisor can help ensure you’re not missing out on savings – or triggering penalties.

Did You Know?

- You can claim the QBI deduction even if you take the standard deduction.

- The deduction is set to expire after 2025 unless Congress takes action to extend it.

- Rental income may qualify for the qualified business income deduction if your rental activity is substantial enough to count as a business.

- The deduction applies only at the federal level — though some states may offer their versions.

Conclusion

The deduction for qualified business income is one of the most impactful tax-saving tools available to U.S. small business owners – but it’s also one of the most misunderstood.

If qualified, this deduction could potentially reduce taxable income by up to 20% freeing up cash to reinvest into the business, to provide a cushion, or simply to save more of what you are earning.

Orbit Accountants helps owners like you take advantage of every opportunity in the tax code-without the muddle. We support you-from start to scale in staying compliant and keeping your finances working in your favor.

Ready to take full advantage of the QBI deduction? Let’s schedule your free consultation.

Frequently Asked Questions:

How do I calculate my QBI deduction?

Take 20% of your qualified business income or 20% of your taxable income minus capital gains — whichever is less. Above income limits, W-2 wage, and property value limits may apply.

Who qualifies for the QBI deduction?

Anyone with pass-through income from a qualified U.S.-based business structure (sole proprietorship, partnership, S corp, etc.) whose income is below the IRS threshold. Above that, phaseouts and limits may apply.

What is the 2.5% rule or 2/7 rule?

The 2.5% rule applies to high-income earners. It’s part of the limitation formula: 25% of W-2 wages plus 2.5% of the unadjusted basis of business property (UBIA).

Is QBI based on adjusted gross income (AGI)?

No. QBI is calculated from your business’s net profit, but your eligibility for the deduction is based on your taxable income, which is derived after AGI.

Which taxes can be reduced by QBI?

The QBI deduction only reduces federal taxable income. It does not reduce self-employment tax or payroll taxes.

What are the limitations on QBI wages?

If your income is above the threshold, your QBI deduction may be limited to 50% of W-2 wages, or 25% of W-2 wages plus 2.5% of UBIA. These wage limitations are meant to tie the deduction to real employment or capital investment.