")

Table of Contents

Why Bookkeeping Matters More Than Ever

Every sale, refund, and payroll run leaves a paper—or digital—trail. If those trails don’t end up in a tidy general ledger, they turn into stress at tax time, patchy insight during the year, and painful cash-flow surprises. U.S. small-business owners face rising compliance rules, from new 1099-K thresholds to evolving state sales-tax filings. Clear, up-to-date records aren’t a “nice-to-have;” they’re the difference between confident growth and late-night panic.

Are you currently managing your bookkeeping in-house?

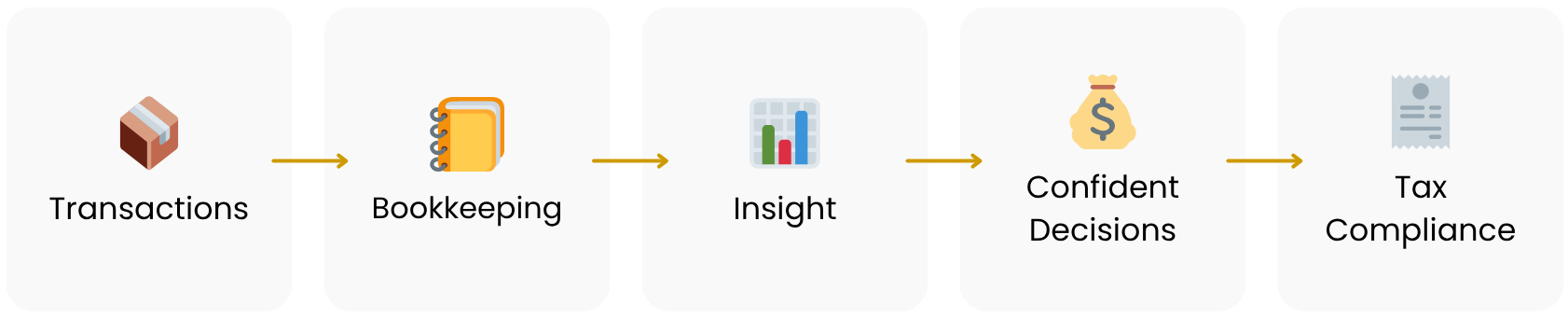

What Exactly Is Book Keeping?

| Term | Plain-English Meaning | Why You Care |

| Chart of Accounts | Master list of buckets for your money (sales, rent, bank fees). | Keeps records consistent. |

| General Ledger | The running story of every dollar in or out. | Creates trusted financial information. |

| Recording Financial Transactions | Writing down sales, bills, and payroll in that ledger. | Forms financial data for decisions. |

| Bank Reconciliation | Matching the books to your bank statement. | Spots errors or fraud fast. |

Sprinkle these concepts into your day-to-day routine and you’ll speak the same language as lenders, investors, and the IRS.

DIY Bookkeeping: The Appeal and the Catch

At first, doing everything yourself feels thrifty. You know every transaction, cash is tight, and free spreadsheets look tempting. Simple bookkeeping software like QuickBooks Online or Wave sweetens the deal with dashboards and bank feeds. Yet three blind spots lurk:

- Time Tax — Even at 3 hours a week, that’s 156 hours a year you could spend selling, networking, or resting.

- Error Risk — A single mis-categorized expense can snowball into bad profit numbers, leading to wrong-size inventory orders or missed tax deductions.

- Compliance Gaps — The IRS expects clear records that “show income and expenses.” Missed receipts today can trigger penalties tomorrow. IRS

How Much Does DIY Really Cost?

| Scenario | Out-of-Pocket | Hidden Cost | Total Pain |

| Spreadsheet Only | Free | 6 hrs/month of owner time ($60/hr opportunity cost) = $4,320/yr | High error rate, no audit trail |

| Basic Software | $300 – $720/yr | Same 6 hrs/month plus software learning curve | Moderate |

| Cleanup After a Mess | $0 upfront | Catch-up bookkeeping firms charge $1,000 – $5,000 for one-time fixes | Very high |

Hiring an in-house bookkeeper runs about $47,000/year plus benefits QuickBooks. Outsourced U.S. bookkeeping services average $300 – $2,500/month depending on transaction volume. Compare those figures to your hidden costs before ruling them out.

Three Roads Forward

I. Spreadsheets

They still work when your side-hustle sells ten candles a week, but watch scope creep: the moment you juggle payroll, inventory, and more than one business bank account, spreadsheet “bookeeping” (yes, the misspelling pops up often!) turns into a maze of hidden formulas. Even the most diligent small-business owner risks skipped bookkeeping tasks such as reconciling each bank statement or tagging every tiny business expense.

II. Simple Bookkeeping Software

Cloud tools like QuickBooks Online or Wave now bundle mileage trackers, receipt capture, and tax-time dashboards. They can feel like the best accounting for small business because they digest feeds instantly and keep bookkeeper records tidy. Look for plans that let you bolt on payroll and sales-tax add-ins as the business grows. Pro tip: test two providers side-by-side for a week; switching later is harder than you think.

III. Hiring a Bookkeeper

A seasoned pro turns messy data into decision-ready financial information. They fine-tune your chart of accounts, verify the general ledger, and flag anomalies before audit letters arrive. Many offer tiered packages: DIY bookkeeping software review only, full monthly close, or controller-level forecasting. Outsourcing even ten hours a month frees you to sell, innovate, or rest—while someone else handles precise recording of financial transactions day-to-day.

When Your Business Outgrows “Shoebox” Accounting

- Your monthly transactions top 200.

- You open a second location or e-commerce channel.

- You hire staff or issue 1099s.

- Investors request GAAP-compliant statements.

- Tax season triggers dread—not clarity.

If two or more apply, it’s time to hire a bookkeeper or upgrade software before mistakes multiply.

Day-to-Day Bookkeeping Checklist (Print This!)

| Daily | Weekly | Monthly | Quarterly |

| Log cash sales | Reconcile bank feeds | Close the general ledger | Review chart of accounts for stale codes |

| Capture receipts | Pay vendor bills | Generate profit & loss | Adjust for depreciation |

| Match merchant fees | Record payroll | File sales-tax returns | Meet CPA for tax-planning |

IRS & GAAP Compliance Tips for U.S. Owners

- Keep source docs (invoices, mileage logs) as long as they affect a filed return. The IRS gives no pass on “lost receipts.” IRS

- Separate personal and business bank accounts to protect your limited liability and simplify audits.

- Use accrual accounting when inventory tops $1 million or investors demand it.

- Lock prior periods in your accounting system after the CPA signs off—reduces accidental edits.

Starting a Bookkeeping Business (For the Curious Reader)

Bookkeeping itself can be a profitable side gig. Here’s a quick blueprint:

- Get trained. Free SBA webinars cover bookkeeping basics Small Business Administration.

- Choose a niche. Retail, creatives, or SaaS all need different chart-of-accounts templates.

- Register an LLC and business bank accounts to separate liability.

- Pick simple bookkeeping software for client work—QuickBooks Online is industry standard.

- Market online through LinkedIn groups for small-business owners or local chambers.

- Charge by transaction volume or fixed monthly packages.

Pro tip: AIPB certification boosts trust when you pitch prospects.

Conclusion — Keeping Your Financial Story Straight

Bottom line: no single path fits every entrepreneur. The right mix of spreadsheets, software, and human help changes as transaction volume, regulation, and ambition rise. Start lean, but revisit your business bookkeeping setup each quarter. Clear, up-to-date books make funding talks smoother, unlock smarter pricing decisions, and turn dreaded tax season into a routine file-and-forget. Remember, consistent, disciplined bookkeeping bookkeeping—however you spell it—secures the financial story you’ll share with partners, lenders, and the IRS tomorrow.

Frequently Asked Questions

What is book keeping in simple terms?

Book keeping is the day-to-day process of recording and classifying every dollar your business earns or spends so you can see profit, pay taxes, and plan growth.

Do I need separate business bank accounts?

Yes. Mixing personal and business funds muddles your general ledger and can pierce liability protections.

Can I handle small business bookkeeping myself?

You can, but budget at least three hours a week and plan to learn IRS rules. Once you hit 200+ monthly transactions or hire staff, consider software or a bookkeeper.

What’s the best accounting system for beginners?

QuickBooks Online is popular for its large support community, but Wave and Zoho Books offer low-cost options. Start with whichever lets you link bank feeds and customize your chart of accounts.

Legal Disclaimer

This article provides general educational information and is not legal, tax, or accounting advice. Consult your CPA or attorney for guidance tailored to your situation. Orbit Accountants and the author assume no liability for actions taken based on this content. All figures and rules are based on U.S. regulations current as of July 2025.