Table of Contents

Introduction

Accounting might sound basic. Account balance errors do occur, even with the best. Leaving out one entry, switching two numbers, or leaving out a receipt can turn an orderly ledger into a confusing mess.

Good thing: accounting errors are mostly avoidable upon knowing the red flags and how to put them right.

The hours, money, and stress saved by being aware of accounting problems and how to prevent them will be beneficial for small business owners, as well as people supervising larger teams.

Are you currently managing your bookkeeping in-house?

What is an Accounting Error?

An accounting error is simply recording common financial errors in transactions. These mistakes can occur in journal entries, ledgers, or even financial statements. Sometimes these are simple typos – like inputting 500$ instead of 50$. At other times, such an error can be the result of misunderstanding accounting principles or posting transactions in an inappropriate account.

Even a minor error could significantly distort your financial health. Making an enterprise decision upon incorrect data is very much like attempting to orient oneself with a misleading map. One must catch mistakes early with the assurance of having pristine reports so that correct decisions may be made.

Common Types of Accounting Errors

Accounting errors come in many forms, and each can affect your books differently. Here are the main ones to watch out for:

Error of Original Entry

This happens when the wrong amount is recorded at the start. For instance, entering $700 instead of $70. Small slip-ups like this can create bigger problems down the line.

Error of Omission

Ever forget to record a transaction entirely? That’s an omission. Even a single missing entry can make your financial statements misleading.

Error of Commission

This is when the right amount goes into the wrong account. Paying for electricity but recording it as rent is a typical example. It’s easy to overlook, but it can skew reports.

Error of Principle

These errors break the rules. Such an error might involve crediting an expense for a building purchase instead of recording it as an asset. Accounting mistakes like this can create tax implications and misrepresent the company’s value.

Error of Duplication

Duplicate entries inflate numbers. Manual bookkeeping is particularly prone to this.

Transposition Error

Sometimes, digits get swapped. $540 instead of $450 is a simple example, but it’s enough to cause discrepancies.

Error of Entry Reversal

The confusion caused by wrongly entered debit or credit entries often results in financial statements with an unbelievably distorted picture.

Compensating Errors

These types of errors in accounting are sneaky. Two errors cancel each other out, so the books seem balanced, but the underlying mistakes still exist.

Examples of Common Accounting and Bookkeeping Mistakes

Accounting errors, while common, do abound even for seasoned bookkeepers. Some common accounting errors include:

- Misclassifying expenses, like posting office supplies as a capital expense.

- Skipping bank reconciliations for months.

- Forgetting small transactions, which could add up rather quickly.

- Posting transactions in the wrong month or year.

- Not updating assets or inventories immediately.

- Not keeping receipts or any documentation organized.

At first, those may seem like such trifling matters, but combined, they can paint a false picture regarding your financial ability and the difficulty of filing your taxes.

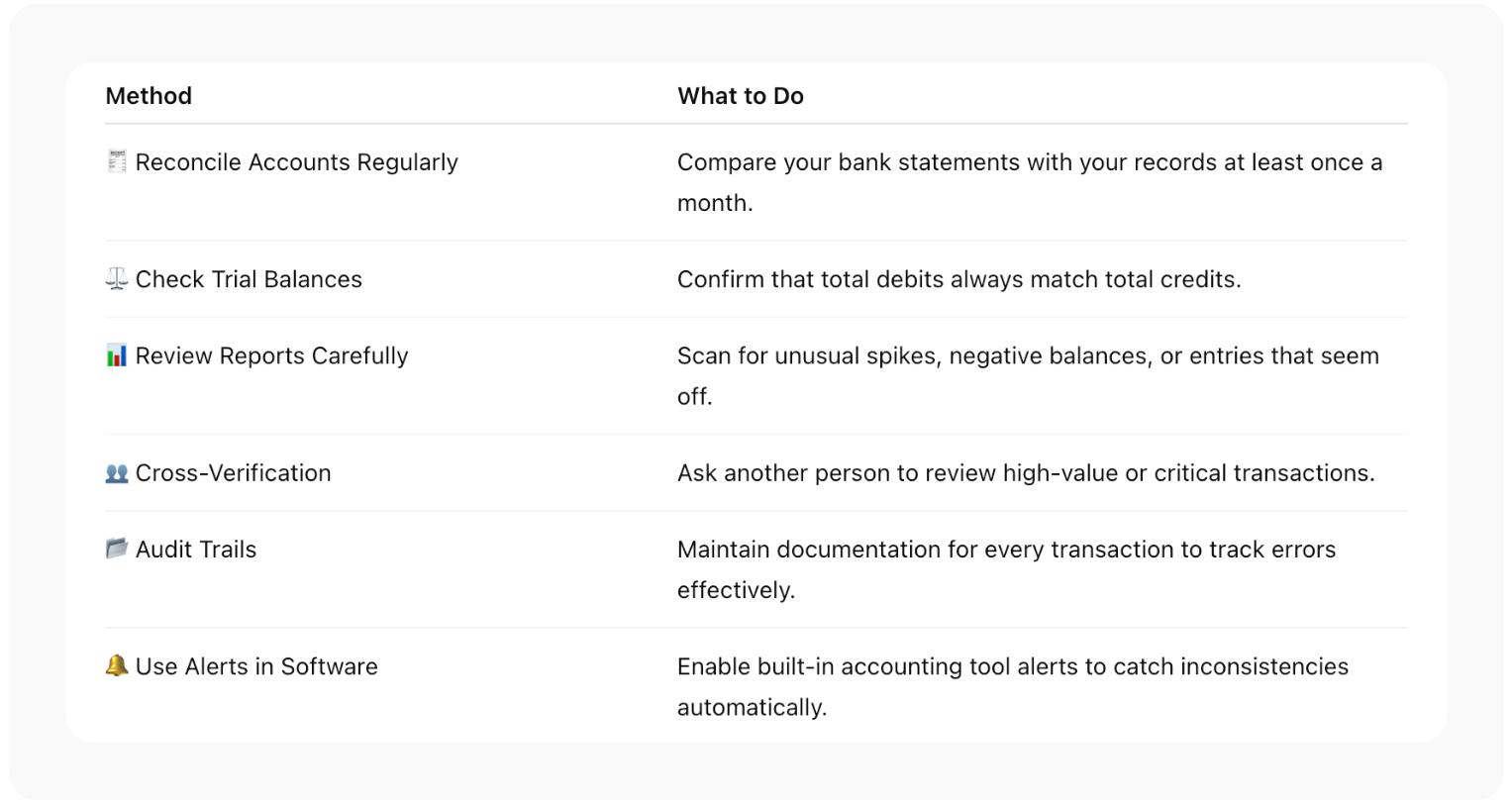

How to Detect Accounting Errors

Catch them early. Here are some practical methods for catching errors:

Practical Ways to Avoid Accounting Errors

Prevention beats correction every time. Here is what works:

Use Accounting Software: Automation eliminates human errors.

Set Standard Procedures: Providing clear guidelines regarding recording transactions should prevent confusion.

Provide Training to Your Team: Any person working with books shall have basic accounting knowledge.

Do Internal Audits at Regular Intervals: Small audits help detect an error before it turns into a major error.

Proper Documentation: Receipts, invoices, any proof of transaction shall be maintained to work on prompt account reconciliation.

Double-Check High-Value Transactions: It is always safer to give the review twice.

A successful integration of these procedures will mean fewer errors and more reliable financial reports.

The Cost of Ignoring Accounting Errors

Ignoring accounting errors is risky. Problems can include:

- Misleading financial statements affect critical decisions.

- Tax penalties and fines due to inaccurate filings.

- Cash flow issues from untracked or misrecorded expenses.

- Loss of credibility with investors, lenders, or partners.

- Stress and wasted time correcting compounded mistakes later.

Sometimes small errors may spiral into a larger problem if the same are not addressed.

Conclusion

If you own a business, accounting errors coming your way are highly possible. But making these errors the sole reason to hamper your business could be the worst.

Good practices, straightforward processes, and current resources will assist you in preventing any errors altogether. Accurate books not only create better decision-making for your business, but also demonstrate to your stakeholders that you have their best interests in mind with their money, in addition to being compliant.

Always remember that keeping your books organized while you clean them up is good business mindset, organized accounting, and proper accounting evaluations are about clarity, organization, and peace of mind; it is not only about the number.

Don’t let accounting problems slow down your business growth. Orbit Accountants simplifies your books, and gives you clear insights to make better and profitable financial decisions.

Frequently Asked Questions

How can I detect accounting errors early?

Monthly reconciliations, reviewing the trial balance, and cross-verifications of entries help detect errors before they contaminate reports.

What is an error of principle in accounting?

It takes place when a transaction is in violation of accounting rules, for instance, recording a capital purchase as an expense.

What are compensating errors?

Errors in pairs may cancel each other; although the balance appears to be correct, the original errors still remain.

How can businesses avoid common bookkeeping mistakes?

Use accounting software, ensure all employees have been trained, standardize best practices, and conduct frequent account reviews.

Why is it important to correct accounting errors promptly?

Errors left uncorrected can mislead reports, cause issues with the tax office, and create problems making business decisions.

How do modern technologies help in identifying accounting mistakes?

Accounting software can alert users to inconsistent information, reconcile accounts, and track audit trails – limiting precise data admission pitfalls.

Can small errors affect business decisions?

Yes. Even minor mistakes can accumulate over time, creating distorted financial insights and poor decisions.