When you’re closing the books each month, one critical step can make or break your financial accuracy: adjusting entries.

For business owners and accountants alike, understanding adjusting journal entries isn’t just about ticking boxes for compliance. It’s about making sure your financials tell the real story — not just what’s been paid or received in cash, but what your business has actually earned or owes.

Whether you’re handling your books solo or reviewing with your accountant, this guide will walk you through adjusting entries accounting with clarity and confidence. With the right knowledge and tools, you’ll be able to handle accounting adjusting entries examples that match the complexity of your business.

Table of Contents

What Are Adjusting Entries?

Adjusting entries are journal entries made at the end of an accounting period to update account balances before preparing financial statements. These entries ensure that your income and expenses are recorded in the correct period, not when cash changes hands, but when the transaction occurs.

In simple terms, adjusting entries align your books with the accrual basis of accounting, where revenues and expenses are matched to the period they belong to. This is where knowing the types of adjusting journal entries and when to apply them becomes essential.

Are you currently managing your bookkeeping in-house?

Why Are Adjusting Journal Entries So Important?

Because no one wants a misleading profit and loss report.

Without adjusting entries, your financials can be off. Revenue you’ve earned might be missing, or expenses might be overstated. That could affect decisions about cash flow, tax planning, and future investments.

Quick Tip for You:

Before finalizing monthly or yearly financials, always check for any required adjusting entries — especially for prepaid expenses, accrued income, or depreciation. These are some of the most common accounting adjusting entries examples you’ll deal with.

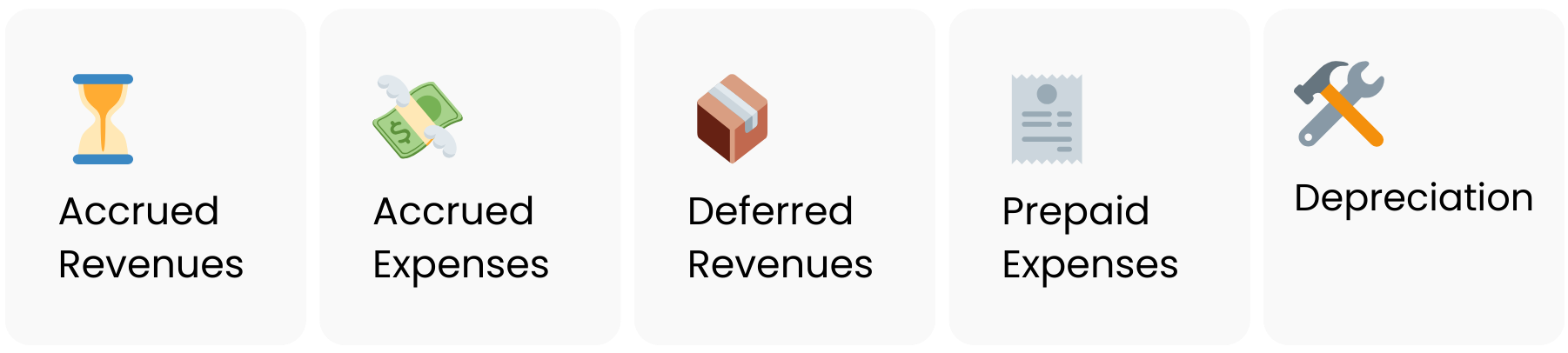

The 5 Main Types of Adjusting Entries (With Examples)

Let’s break down the core adjusting entries accounting requires. You’ll see these pop up regularly if you’re managing bookkeeping under the accrual system.

1. Accrued Revenues

These are revenues earned but not yet received or recorded. Accrued revenues typically arise when services are provided near the end of the accounting period, but the invoice hasn’t gone out yet.

Example: You completed a project worth $5,000 on July 30 but haven’t invoiced the client yet.

Adjusting Journal Entry:

| Account | Debit | Credit |

| Accounts Receivable | $5,000 | |

| Service Revenue | $5,000 |

2. Accrued Expenses

Accrued expenses are costs that your business has incurred during a period but hasn’t yet paid. Common examples include wages, interest, or utilities that are due after the accounting period ends.

Example: You owe $1,000 in wages for July, payable in August.

Adjusting Journal Entry:

| Account | Debit | Credit |

| Wage Expense | $1,000 | |

| Wages Payable | $1,000 |

3. Deferred Revenues

Deferred (or unearned) revenues occur when a customer pays you in advance for services you haven’t yet performed. Over time, as you deliver the service, revenue is recognized.

Example: A client paid you $2,000 in advance for a two-month subscription starting next month.

Adjusting Journal Entry:

| Account | Debit | Credit |

| Unearned Revenue | $1,000 | |

| Service Revenue | $1,000 |

4. Prepaid Expenses

Prepaid expenses are payments made in advance for goods or services to be received in the future. As time passes, the portion used becomes an expense.

Example: You paid $1,200 for annual insurance in January. Each month, you need to spend $100.

Adjusting Journal Entry:

| Account | Debit | Credit |

| Insurance Expense | $100 | |

| Prepaid Insurance | $100 |

5. Depreciation

This is one of the classic accounting adjusting entries examples, showing how asset value spreads over time.

Example: You bought equipment for $12,000 with a 5-year life. Monthly depreciation is $200.

Adjusting Journal Entry:

| Account | Debit | Credit |

| Depreciation Expense | $200 | |

| Accumulated Depreciation | $200 |

Understanding the Pattern of Adjusting Entries

Though every business is unique, adjusting entries typically follow a predictable pattern:

- They occur at the end of an accounting period.

- They involve at least one income or expense account.

- They often work with asset or liability accounts like Prepaid Expenses or Unearned Revenue.

They never touch the cash account.

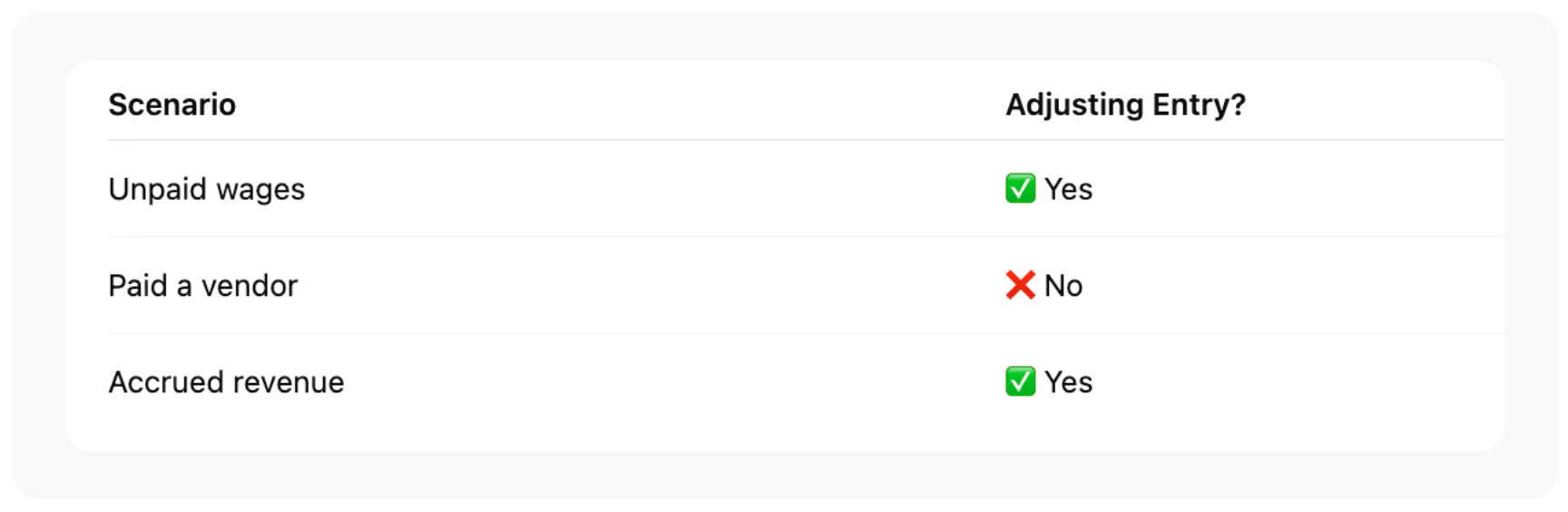

Why Adjusting Entries Never Affect Cash?

This is a golden rule in accounting: Adjusting entries do not involve cash.

Why? Because cash is recorded when it moves. Adjusting journal entries, however, handle the things that haven’t yet happened in terms of cash, like unpaid bills or earned income you haven’t invoiced yet. These entries adjust the timing to ensure everything is recorded in the correct period, even if the cash hasn’t changed hands yet.

For example, if you’ve finished a service in March but won’t invoice until April, the revenue needs to be recognized in March, not when the payment comes in. Similarly, if you prepaid for insurance, each month you need to recognize a portion of the cost, even though you paid it up front.

So if you see an entry involving the Cash account during your month-end adjusting process, double-check. That’s likely a regular transaction, not an adjusting one.

Rules to Keep in Mind

When dealing with adjusting entries, consistency and timing are everything. Here are the basic rules to always follow:

- Only make them at the end of an accounting period. These entries are part of your closing process, not something you do daily.

- Stick to accrual accounting. The whole point is to match income and expenses to the period they happened, not when the cash came in or went out.

- Never touch the cash account. If cash is involved, it’s not an adjusting entry. Simple as that.

- Keep things documented. Every adjustment should have a clear explanation behind it—what it’s for, how you calculated it, and why it’s needed. It keeps your records clean and audit-ready.

Conclusion:

Adjusting entries might seem like small end-of-period tasks, but they shape the foundation of every financial report. When they’re skipped or done incorrectly, the consequences echo across tax filings, audits, and financial strategy.

But when they’re handled with precision? You gain full clarity — the kind that leads to smarter decisions and stronger growth.

Not sure if your books need adjusting? Or want to be 100% confident before your next tax filing or stakeholder meeting?

Let us take a look.

Our accounting pros at Orbit Accountants specialize in spotting what your books may be missing — from overlooked adjusting entries to strategic tax-saving opportunities.

Book a free consultation now and ensure your numbers tell the full story.

Frequently Asked Questions:

What are the 5 main adjusting entries?

The main among them are accrued revenues, accrued expenses, deferred revenue, prepaid expense, and depreciation, so your income and expenses reflect the correct period accurately.

What are the main rules for adjusting entries?

Adjusting entries never involve cash; they are made at the end of the period and follow accrual accounting, and they must be documented for accuracy.

What is the pattern of adjusting entries?

Adjusting entries are typically for one income or expense account and one balance sheet account, and are typically recorded just before preparing financial statements or closing your books.

Why do adjusting entries never affect cash?

It deals with income earned or expenses incurred, but cash is not transacted – cash is always recorded in a separate field.